Ice storms can bring business operations to a sudden halt. Ice buildup can damage roofs, freeze pipes, and knock out power, leaving commercial properties unable to operate for days. The financial impact can escalate quickly, from lost income to ongoing expenses that don’t stop just because your business does.

During the 2021 Texas Winter Storm Uri, more than 4.5 million properties lost power, and economic losses reached an estimated $80 to $130 billion. Louisiana also saw over 150,000 outages during the same event, disrupting businesses across the region. For many business owners, these disruptions can quickly turn into complex insurance and recovery challenges. When losses escalate at this scale, understanding your coverage and next steps becomes critical to protecting your business. This guide explains how ice storm business interruption claims work, what your policy may cover, and the challenges business owners often face when pursuing recovery.

What Business Interruption Insurance Covers for Ice Storm Damage

Business Interruption (BI) insurance is designed to help cover financial losses when your business cannot operate due to covered property damage. When it comes to ice storms, coverage typically begins when there is direct physical damage to your commercial property caused by ice, such as roof collapse, frozen pipes, or structural damage. Without this physical damage trigger, many policies may not apply.

Once triggered, a business interruption claim may include:

- Lost net income, based on what your business would have earned if operations had continued normally.

- Ongoing operating expenses, such as rent, payroll, and utilities that continue even during a shutdown.

Extra expenses, including costs for temporary relocation, generator use, or urgent repairs to resume operations sooner

Key Coverage Extensions Relevant to Ice Storms

Many policies also include extensions that become especially important during ice-related events, such as:

- Service or utility interruption, which may apply when ice damages power lines or infrastructure supplying your business.

- Contingent business interruption, covering losses caused by disruptions to key suppliers or vendors.

- Ingress and egress, when ice or debris prevents access to your property.

- Civil authority, when the government orders restrict access to your business due to unsafe conditions.

In some cases, businesses may explore support from programs like FEMA or SBA disaster loans. However, these options typically supplement insurance recovery rather than replace a business interruption claim.

Types of Ice Storm Damage That Lead to Business Interruption

Ice storms can affect commercial properties in multiple ways, often triggering complex ice storm BI claims. The type and extent of damage play a critical role in determining whether business interruption coverage applies and how losses are evaluated.

Structural Ice Damage

Heavy ice accumulation can place extreme stress on building structures, especially when weight builds up over time. In many cases, this type of damage is not immediately visible but can quickly lead to unsafe conditions that force a shutdown.

For example:

- Roofs may sag or collapse under the weight of accumulated ice.

- Ice dams can form along roof edges, allowing water to seep into ceilings and walls.

- Exterior elements such as windows, façades, and signage may crack or detach.

Even partial structural damage can interrupt normal operations while inspections and repairs take place.

Frozen and Burst Pipes

When temperatures drop rapidly, water inside pipes can freeze and expand, leading to sudden pipe failures. This type of damage often escalates quickly and affects multiple areas within a property. As a result:

- Burst pipes can flood interior spaces, damaging flooring, walls, and fixtures.

- Water intrusion may require cleanup, drying, and restoration before reopening.

- Critical systems may need to be shut down until repairs are completed.

For many businesses, this becomes a key driver of ice storm BI claims, particularly when operations cannot resume immediately.

Power Outages and Utility Failures

Ice storms frequently damage power lines and transformers, cutting off essential utilities. During the 2021 winter storm, millions of properties across Texas, Louisiana, and nearby regions experienced extended outages, demonstrating the scale of disruption these events can cause.

In practical terms:

- Loss of electricity can halt production, sales, and day-to-day operations.

- Perishable goods may spoil during prolonged outages.

- Communication, security, and IT systems may also be affected.

Even without visible structural damage, a sustained loss of power can bring business activity to a standstill.

Equipment and Inventory Damage

In addition to structural issues, ice storms can directly impact equipment and inventory. These losses may not always be immediately obvious, but they can significantly affect operations and revenue.

For instance:

- Temperature-sensitive inventory, such as food or pharmaceuticals, may degrade or spoil.

- Machinery can malfunction or fail when exposed to freezing conditions.

- Sudden temperature fluctuations may damage sensitive systems or materials.

These types of losses often increase the overall financial impact of ice storm business interruption claims.

Access and Operational Disruptions (Ingress/Egress)

In some situations, the disruption is not limited to the property itself. Ice-covered roads and hazardous conditions can make it difficult or unsafe to access the business. This can affect both customers and employees, as well as supply chains.

For example:

- Blocked or unsafe roads may prevent access to the property.

- Deliveries and vendor services may be delayed or halted.

- Local authorities may restrict movement due to safety concerns.

Businesses in Gulf Coast regions, including Louisiana and Texas, often face additional recovery challenges due to infrastructure limitations and supply chain delays following severe weather events.

Understanding how these different types of damage impact operations can help clarify when and how ice storm BI claims may apply.

Step-by-Step Process to File an Ice Storm BI Claim

Filing an ice storm business interruption claim involves more than simply reporting property damage. It requires timely action, clear documentation, and a structured approach to demonstrating both physical damage and financial loss. Taking the right steps early can help reduce complications during the claims process.

1. Notify Your Insurance Provider Immediately

The first step is to notify your insurance provider as soon as possible after the loss. Most policies include strict reporting requirements, and delays can complicate the claims process. Early notice helps establish a clear timeline and allows the insurer to begin evaluating the claim.

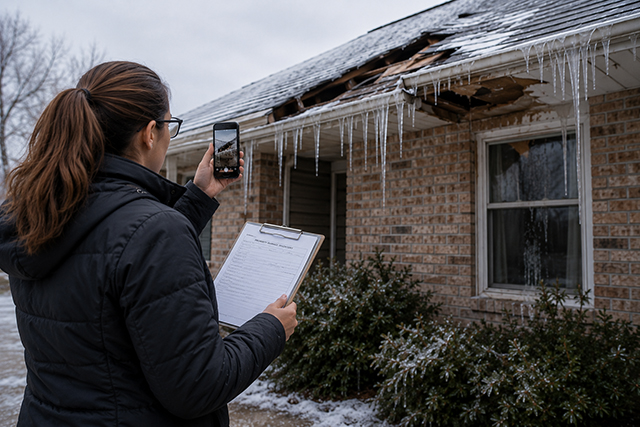

2. Document All Ice-Related Damage

Once it is safe to do so, focus on documenting all visible damage. This step plays a critical role in supporting your claim and connecting the loss to the ice storm event.

In practice, this means you should:

- Take clear photos and videos of ice buildup, structural damage, and affected areas.

- Capture evidence of burst pipes, water intrusion, and damaged equipment.

- Record the condition of your property as soon as possible after the storm.

Strong documentation can help minimize disputes later in the process.

3. Take Steps to Prevent Further Damage

Most policies require you to take reasonable steps to prevent additional damage. These mitigation efforts not only protect your property but also demonstrate compliance with policy obligations.

For example, you may need to:

- Make temporary repairs, such as covering damaged roofs or securing openings.

- Remove standing water or ice to prevent further deterioration.

- Keep detailed records and receipts for all mitigation work.

These actions can help support your position when the claim is reviewed.

4. Gather Financial Documentation

To support an ice storm business interruption claim, you will need to demonstrate the income your business would have earned if the disruption had not occurred. This requires organized and accurate financial records.

Typically, this includes:

- Profit and loss statements from at least two prior years

- Payroll records, tax filings, and ongoing expense documentation

- Financial data reflecting normal business operations before the storm

This information forms the basis for calculating your lost income.

5. Track Extra Expenses

In addition to lost income, many policies cover extra expenses incurred to maintain or restore operations. Keeping detailed records of these costs is essential.

Be sure to:

- Document expenses related to temporary relocation or alternate workspaces.

- Track costs for equipment rentals, generators, and emergency services.

- Maintain organized records to support reimbursement requests.

Accurate tracking can help ensure these expenses are properly considered.

6. Obtain a Licensed Contractor Estimation for Damages

A professional damage assessment can strengthen your claim by clearly documenting the extent of physical loss. Working with a licensed contractor can help you establish a reliable estimate and support your claim valuation.

7. Work with Ice Storm Claim Expert

If complications arise, it may be helpful to seek guidance from a property damage attorney. They can assist with interpreting policy language, addressing delays or denials, and helping you navigate the complexities of ice storm business interruption claims.

By following a structured approach and maintaining thorough records, you can strengthen your claim and better navigate the challenges that may arise.

Common Challenges and Reasons Ice Storm BI Claims Are Denied

While many policies provide coverage for business interruption, ice storm BI claims are often disputed or denied due to specific policy requirements and interpretations. Understanding these challenges can help business owners better prepare and respond.

- No Direct Physical Damage: Insurers may deny claims if they determine that operations were disrupted without clear, documented physical damage caused by the ice storm. For example, a business that closes due to extreme cold or precautionary shutdowns may face challenges if no structural or tangible damage is documented.

- Maintenance or Negligence Allegations: Carriers may argue that the damage resulted from a lack of upkeep, such as failing to winterize pipes or maintain roofing systems, rather than the ice storm itself.

- Waiting Period Limitations: Most policies include a waiting period, typically 24–72 hours, before business interruption coverage begins. Losses during this initial period may not be covered, which can reduce the total recoverable loss, especially for shorter disruptions.

- Utility Interruption Restrictions: Coverage may depend on where the damage occurred. If ice damages power infrastructure away from your property, insurers may limit or deny portions of the claim.

- Flood vs. Ice Damage Disputes: When ice melts and causes water intrusion, insurers may classify the damage as flood-related, which is often excluded under standard policies.

- Underpayment or Loss Valuation Disputes: Disagreements frequently arise over how lost income is calculated, what expenses qualify, and how long recovery should reasonably take.

Recognizing these challenges can help you better prepare your documentation and strengthen your position when pursuing an ice storm business interruption claim.

How an Ice Storm Damage Claim Attorney Can Help

Handling ice storm BI claims can become complicated, particularly when disputes arise over coverage or valuation. Working with an experienced ice storm claim expert or a property damage attorney can provide clarity and support throughout the process.

An ice storm damage insurance claim attorney can help you with:

- Reviewing Policy Terms and Coverage Details: An attorney can carefully review your policy to identify applicable coverage, exclusions, and extensions, helping you understand what your claim may include.

- Supporting Claim Documentation and Loss Calculation: They can assist in organizing evidence of physical damage and financial loss, ensuring your claim is supported with clear and accurate documentation.

- Handling Insurance Company Negotiations: When communication becomes challenging, an attorney can step in to address delays, inconsistencies, or requests for additional information.

- Challenging Denials or Delays: If your claim is denied or underpaid, they can evaluate the reasoning and respond based on the policy language and supporting evidence.

- Maximizing Claim Recovery: By identifying overlooked areas of coverage and strengthening your claim presentation, an attorney can help position your claim more effectively.

Having the right legal guidance can make a meaningful difference when navigating coverage disputes and claim-related issues. With the stakes often high, having someone who understands the process can help you move forward with greater clarity and confidence.

Conclusion

Ice storms can create sudden and complex disruptions, making it essential to understand how coverage applies and what triggers a valid claim. Acting quickly, documenting damage thoroughly, and maintaining clear, well-organized financial records can significantly impact how your claim is evaluated.

Given the coverage issues and disputes that often arise with ice storm business interruption claims, having experienced legal guidance can help you better navigate policy terms, address disputes, and protect your business’s path to recovery.

If you’re unsure where your claim stands, a free claim review from Pandit Law can help you better understand your options and take informed next steps.

Frequently Asked Questions

Ice storm damage may be covered if it causes direct physical damage to the insured property. Coverage typically depends on your policy terms, including specific inclusions, exclusions, and any applicable coverage extensions related to ice or winter storm events.

A business interruption claim is usually triggered when an ice storm causes direct physical damage that forces your business to suspend operations. This can include structural damage, frozen or burst pipes, utility failures, equipment damage, or operational disruptions. However, the inability to operate must be directly linked to covered damage under your policy.

You can support your claim by providing clear evidence of damage along with records that demonstrate the financial impact of the interruption on your operations. Evidence such as photos, repair estimates, and income records helps connect the loss directly to the ice storm event.

Ice storm damage often involves freezing, weight buildup, and water intrusion, while snow-related damage may involve accumulation without freezing impact. Coverage depends on how the policy defines and distinguishes between these types of weather-related events.

Power outages may be covered if they result from covered physical damage, either on your property or, in some cases, nearby utility infrastructure. Coverage often depends on specific policy provisions, such as utility interruption or service-related extensions.