Whether a hurricane tears through your neighborhood, a fire damages your home, or a burst pipe disrupts your business, it’s often difficult to know what to do next. And before you can even think about repairs, you’re suddenly trying to protect your property, document the damage, and figure out what your insurance policy expects you to do next.

Most property insurance policies include a Duties After Loss clause that outlines the steps policyholders must take after a covered loss. These contractual obligations are separate from the insurance company’s responsibilities, and failing to meet them can lead to delays or disputes during the claims process.

This guide explains each post-loss duty, common mistakes to avoid, key legal considerations in Louisiana and Texas, and when a property damage attorney may be able to help.

Your Post-Loss Duties as a Policyholder: What Your Insurance Policy Requires

Most homeowners and commercial property insurance policies include a Duties After Loss clause that outlines what you must do after a covered loss. These guidelines can help preserve evidence, support the insurer’s investigation, and protect your right to recover under your policy.

While every policy differs, the following responsibilities appear in most property insurance policies:

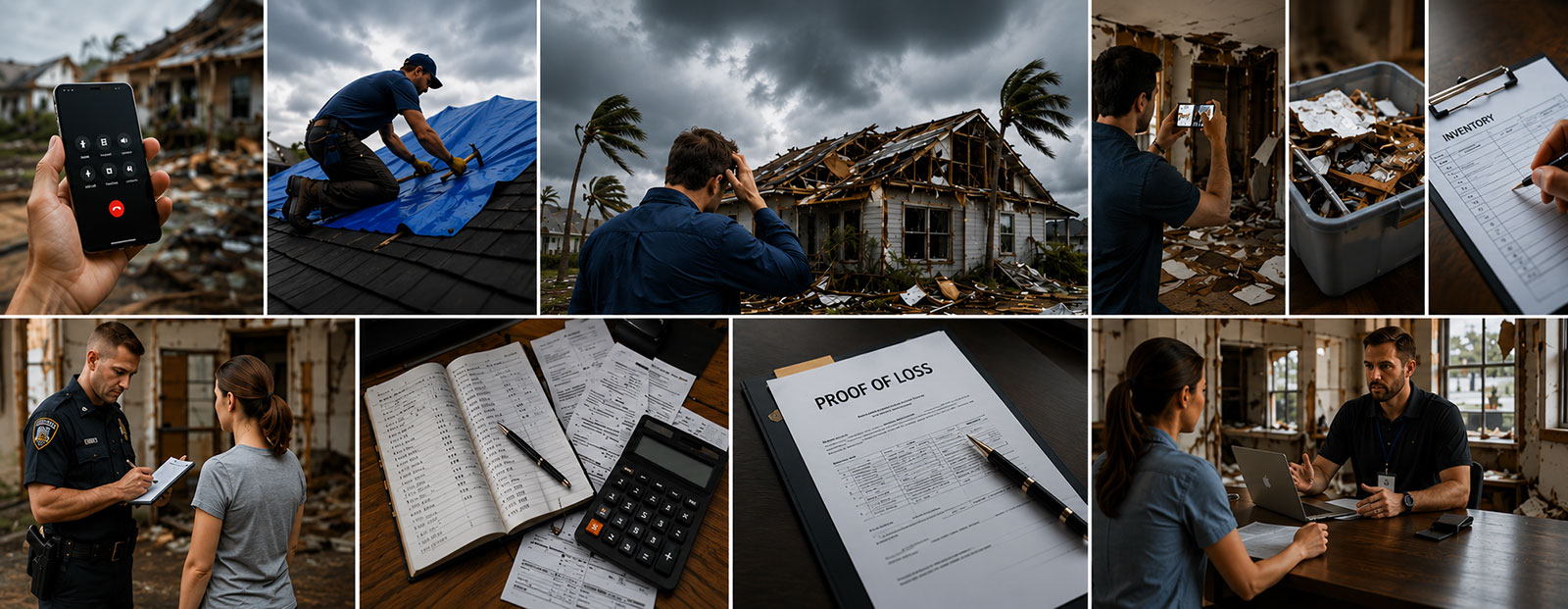

Notify Your Insurance Company Promptly

Report the damage as soon as reasonably possible after discovering it. Early notice gives the insurer an opportunity to investigate the loss while the evidence is still available and reduces the risk of unnecessary delays.

When reporting the loss, be prepared to provide:

- The date and time of the incident

- The property address or location of the damage

- A brief description of the cause and type of damage

- Your contact information and policy details, if available

Waiting too long to report a claim can complicate the investigation and, in some situations, affect coverage under your policy.

Protect the Property From Further Damage (Duty to Mitigate)

After reporting the loss, take reasonable steps to prevent additional damage. This duty, often called the duty to mitigate, does not require you to restore the property immediately. Instead, it means taking practical measures to keep the damage from getting worse, which may include:

- Placing a tarp over a damaged roof

- Boarding broken windows

- Shutting off the water supply to stop active leaks

- Drying wet areas to limit additional damage

Emergency repairs are generally appropriate, but permanent restoration should usually wait until you’ve documented the damage and the insurer has had an opportunity to inspect the property.

Document All Damage Before Cleanup or Repairs

Before removing debris or beginning repairs, create a thorough visual record of the damage. Good documentation makes it easier to establish the cause of loss and the extent of the damage. Be sure to capture:

- Wide-angle and close-up photos of structural damage

- Damaged personal belongings and affected rooms

- Timestamped or geotagged photos, when available

- A narrated video walkthrough showing the property’s condition

Continue documenting the property if the damage changes before repairs begin.

Preserve Damaged Property and Evidence

Keep damaged materials and property whenever possible until the insurer has completed its inspection. Discarding evidence too early can make it more difficult to verify what was damaged.

If possible, retain damaged items, repair invoices, cleanup receipts, and any other physical evidence that supports your claim until you’re told they are no longer needed.

File a Police Report When Required

Not every property damage claim requires a police report. However, one is generally appropriate when the loss involves theft, burglary, vandalism, or other criminal activity.

Claims involving hurricanes, hail, fires, floods, or other natural disasters typically do not require a police report, although reports from local emergency agencies may still help document the event.

Create a Detailed Inventory of All Damaged Property

A complete inventory helps support the value of your claim and reduces the chance of overlooking damaged items. When creating an inventory, include details such as:

- Item description and quantity

- Estimated age and condition

- Replacement cost, if known

- Available receipts, warranties, or pre-loss photos

Business owners should also inventory damaged equipment, inventory, furniture, and other commercial assets affected by the loss.

Keep Records of All Expenses Related to the Loss

Expenses can add up quickly after a property loss. Save receipts and maintain organized records for emergency repairs, cleanup, temporary housing, meals, storage, and other covered costs. Depending on your policy, homeowners may also have Additional Living Expenses (ALE) coverage, while businesses may have Business Interruption coverage for certain losses.

Keeping everything in one digital or physical claim folder can make it easier to locate documents if questions arise later.

Submit a Proof of Loss (If Requested)

A sworn Proof of Loss is a formal statement that summarizes the damage and the amount you’re claiming under your policy. Unlike your initial claim report, this document is typically submitted only if your insurer requests it.

Review the form carefully before signing. Errors or incomplete information can create unnecessary complications during the claims process.

Cooperate With the Insurance Investigation

Your policy generally requires you to cooperate with the insurer’s investigation by allowing inspections, providing requested records, and responding to reasonable questions. Responding promptly and providing complete information can help keep the investigation moving forward.

In some cases, the insurer may request an Examination Under Oath (EUO), a formal interview conducted under oath. You have the right to legal representation during this process.

Avoid Making Permanent Repairs Without Insurer Authorization

Temporary measures that protect your property are different from permanent restoration. Completing major repairs before the insurer documents the original damage can make it harder to determine what the covered loss included.

At the same time, insurers also have a duty to inspect damaged property within a reasonable period after the claim is reported. Once the necessary documentation and inspections are complete, you can move forward with permanent repairs more confidently.

Understanding and fulfilling these post-loss duties can help reduce unnecessary disputes and keep your claim moving forward.

What Happens If You Don’t Follow Your Duties After Loss?

Meeting your policy’s post-loss requirements is more than a procedural step. It gives the insurer the information needed to evaluate your claim and helps protect your rights under the policy. Failing to meet these obligations can create avoidable complications, such as:

Your Claim Could Be Delayed or Denied

When required information is missing or evidence is no longer available, the insurer may not be able to complete its investigation. This can delay the claims process and, in some cases, result in a denial if the insurer cannot determine whether the loss is covered.

Your Settlement May Be Reduced

The value of a property damage claim depends largely on the evidence supporting it. Missing photos, incomplete inventories, or discarded damaged property can make it more difficult to establish the full extent of the loss. As a result, the settlement offered may not fully reflect the documented damage.

You May Lose the Right to Sue

Many property insurance policies include suit limitation clauses that set deadlines and conditions for filing legal action. Missing policy requirements or waiting too long to act could affect your ability to pursue a dispute later. Reviewing your policy carefully can help you understand these requirements.

Your Payout Can Be Reduced

Even if your claim is approved, failing to cooperate with reasonable requests or provide sufficient documentation may affect the amount ultimately paid. The insurer’s evaluation is based on the available evidence, so complete and accurate records are important throughout the process.

Inaccurate Information Can Lead to Fraud Allegations

Always provide truthful and accurate information when reporting a loss or submitting documents. Honest mistakes can often be corrected, but knowingly providing false or misleading information may raise fraud concerns and complicate your claim.

Understanding these potential consequences highlights why every post-loss duty matters. Taking the right steps from the beginning can help support a smoother claims process and reduce the risk of unnecessary disputes.

Louisiana and Texas: What State Law Says About Duties After Loss

Although your insurance policy outlines your post-loss responsibilities, state laws also establish important deadlines and requirements that affect how insurers handle property damage claims.

Louisiana

- Under La. R.S. 22:1892, insurers generally must initiate loss adjustment within 14 days after receiving notice of a property damage claim and pay amounts due within 30 days after receiving satisfactory written proof of loss.

- For catastrophic property losses, including many hurricane claims, insurers generally must initiate loss adjustment within 30 days after receiving notice of the loss, subject to limited extensions authorized by the Louisiana Commissioner of Insurance during declared emergencies. For catastrophic residential property claims, insurers generally must transmit payment of amounts due within 60 days after receiving satisfactory written proof of loss.

- Louisiana’s Valued Policy Law may also apply to qualifying total losses.

If questions arise during the claims process, a Louisiana property damage claim lawyer can help you understand your legal rights.

Texas

- The Texas Prompt Payment of Claims Act generally requires insurers to acknowledge a claim and request any needed information within 15 days, then make a coverage decision within 15 business days after receiving all required information.

- Once a claim is approved, payment is generally due within 5 business days.

- Some deadlines may be extended under Texas law in certain circumstances.

- Homeowners with windstorm coverage through the Texas Windstorm Insurance Association (TWIA) should also follow its reporting deadlines.

- Texas law also provides protections against certain unfair claim handling practices.

If a dispute develops, a Texas property damage claim attorney can explain your available legal options.

Best Practices for Filing a Homeowners Insurance Claim After Property Loss

Recovering from property damage can feel overwhelming, but the steps you take immediately afterward can have a significant impact on your claim. Following these best practices for filing a homeowners insurance claim can help reduce delays, strengthen your documentation, and minimize the risk of disputes:

Report the Loss Promptly

Contact your insurer promptly and provide the basic information needed to open the claim. This may include the date of the loss, the property address, and a brief description of what happened. Early reporting allows the insurer to begin its investigation while the evidence is still fresh.

Document the Damage

Good documentation should clearly show the condition of the property before cleanup begins. Be sure to:

- Take clear photos and videos from multiple angles.

- Document both structural damage and damaged belongings.

- Keep damaged materials until the insurer has inspected them.

Thorough documentation can make it easier to support the extent of your loss if questions arise later.

Prevent Further Damage

Take reasonable steps to protect your property from additional damage after the loss. Temporary measures, such as covering a damaged roof or stopping an active leak, can help prevent the situation from worsening while you wait for the insurer’s inspection.

Avoid Permanent Repairs

Unless emergency conditions make immediate work necessary, wait until the insurer has inspected the damage before authorizing major repairs. If permanent repairs cannot safely wait, document the damage thoroughly before work begins whenever possible. Also, keep all the invoices and other records related to the repairs explaining why the work could not be delayed.

Keep All Claim Records

Staying organized can make the claims process much easier. Maintain copies of:

- Receipts and invoices

- Repair estimates

- Email correspondence

- Letters from the insurer

- Notes or a log of phone conversations

Having all claim-related documents in one place allows you to respond quickly if additional information is requested.

Understand Your Coverage

Take time to review your policy before accepting a settlement offer. Pay close attention to your deductible, coverage limits, exclusions, and whether your policy provides replacement cost coverage or Actual Cash Value (ACV) coverage. Understanding these terms can help you better evaluate the insurer’s decision.

Review and Negotiate the Settlement

Carefully compare the settlement offer with your documentation. If something appears to be missing or undervalued, ask the adjuster to explain how the amount was calculated. If the offer does not accurately reflect your documented damage, you may be able to negotiate a revised settlement.

Avoid Common Mistakes

Small mistakes can create unnecessary complications during a claim. Avoid things like:

- Exaggerating the extent of the damage

- Discarding damaged property before inspection

- Signing documents you do not fully understand

Taking a careful, organized approach helps protect the integrity of your claim.

Respond to Insurer Requests

Reply promptly to reasonable requests for documents, inspections, or additional information. If the insurer schedules an Examination Under Oath (EUO), cooperate with the process and consider seeking legal guidance before participating.

Seek Legal Help if Needed

If your claim is delayed, underpaid, denied, or becomes disputed, it may be time to speak with a property damage attorney. Legal guidance can help you understand your policy, protect your rights, and evaluate your options without adding unnecessary stress during an already difficult time.

Following these best practices can help you navigate the claims process with greater confidence. If challenges arise despite your efforts, understanding your rights and seeking timely guidance can help you make informed decisions about your next steps.

How a Property Damage Lawyer Can Help You After a Property Loss

Even when you follow every post-loss requirement, disputes can still arise. If your claim becomes delayed, underpaid, denied, or unusually complicated, a property damage attorney can help you understand your rights and protect your interests throughout the claims process.

They can help you:

Keep Your Claim on Track

Insurance policies contain deadlines and documentation requirements that can be easy to overlook after a major loss. An attorney can review your policy, explain your obligations, and help ensure important deadlines and policy conditions are met while addressing issues that could delay your claim.

Strengthen the Evidence

Well-supported claims are often easier to evaluate. An attorney may work with contractors, engineers, accountants, or other qualified professionals to help document the cause, extent, and value of the damage. Strong evidence can be especially important when the insurer disputes the scope of the loss.

Assist With Proof of Loss and EUO

Formal claim procedures require careful attention to detail. If you’re asked to submit a sworn Proof of Loss or participate in an Examination Under Oath (EUO), legal guidance can help you understand the process, prepare accurate information, and avoid unnecessary mistakes.

Challenge Wrongful Delays or Denials

If an insurer delays a claim without justification, underpays documented damage, or denies coverage that you believe should apply, an attorney can review the claim, communicate with the insurer, and explain the legal options available under your policy and state law.

Let You Focus on Recovery

Managing a disputed claim while repairing your home or business can be overwhelming. Having legal support allows you to focus on rebuilding while someone helps protect your rights and addresses claim-related issues on your behalf.

Whether you need answers about your policy or assistance resolving a disputed claim, seeking legal guidance early can help you make informed decisions and move forward with greater confidence.

Post-Loss Duties Checklist for Policyholders

After a property loss, it’s easy to overlook an important step. Use this checklist to help stay organized throughout the claims process:

- Notify your insurer promptly.

- Prevent further damage.

- Document all damage.

- Preserve damaged property and evidence.

- File a police report when required.

- Prepare a detailed inventory.

- Keep all expense records.

- Submit a Proof of Loss if requested.

- Cooperate with the insurer’s investigation.

- Avoid permanent repairs until inspections are complete.

Following these steps can help you meet your policy obligations and reduce avoidable delays or disputes as your claim moves forward.

Conclusion

Recovering from a property loss involves more than repairing the damage. It also means understanding the responsibilities your insurance policy places on you while expecting the insurer to fulfill its obligations under the policy and applicable state law. Taking prompt action, preserving evidence, maintaining accurate records, and responding to reasonable requests can help support a smoother claims process and reduce the likelihood of unnecessary disputes.

If your claim becomes delayed, underpaid, denied, or you have questions about your rights, you don’t have to navigate the process alone. The experienced property damage attorneys at Pandit Law can review your situation, explain your legal options, and help protect your interests.

Contact Pandit Law today for a free case evaluation.