When authorities issue a hurricane warning, most people focus on boarding windows, stocking supplies, and planning where to go. While these steps matter, the aftermath of a storm often creates a different challenge: documenting damage and proving what your policy covers.

The financial impact of a hurricane can be substantial. According to data published by the Office for Coastal Management, 2024 saw 27 billion-dollar disasters, resulting in $182.7 billion in damages. These losses show why hurricane preparedness should go beyond storm safety and include protecting your property and preparing for potential insurance claims before a storm arrives.

Many homeowners know how to prepare for survival, but not what to do before a hurricane to protect their insurance interests. This guide focuses on insurance readiness before landfall and the steps that can help support a property damage claim if a hurricane causes losses. It starts with an often-overlooked step: understanding what your insurance policy does and does not cover before a storm approaches.

Step 1: Review Your Insurance Policy Before a Hurricane Hits

Many homeowners assume they can update their coverage whenever a storm is approaching. In reality, timing plays a major role in what coverage options remain available once hurricane activity begins.

Why Timing Matters More Than Most Homeowners Realize

One of the most important things to understand about what to do before a hurricane is that insurance decisions often become more limited as a storm develops. Once the National Hurricane Center names a storm and it threatens a region, many insurers may impose temporary underwriting restrictions, commonly called moratoriums.

During a moratorium, insurers may restrict:

- New policy purchases

- Coverage increases

- Changes to certain endorsements

- New flood insurance applications or modifications, depending on the policy type and timing

Unfortunately, many homeowners discover these restrictions only after a storm is already approaching. By then, opportunities to adjust coverage may have passed. Reviewing your policy early gives you time to understand your coverage and make informed decisions without the pressure of an incoming storm.

What Your Policy Actually Controls in a Hurricane Claim

Your insurance policy determines far more than whether a claim is covered. It also defines the financial responsibilities and protections that apply after a storm.

Pay close attention to:

- Hurricane or named-storm deductibles, which are often calculated as a percentage of your home’s insured value rather than a fixed dollar amount.

- Dwelling coverage (Coverage A), which helps pay for damage to the physical structure of your home.

- Additional Living Expenses (ALE) (Coverage D), which may help cover temporary housing and related costs if storm damage makes your home uninhabitable.

- Flood-related exclusions, since standard homeowners insurance policies generally do not cover flood damage.

Understanding these provisions before hurricane season can help you avoid surprises when reviewing a future hurricane damage claim.

Step 2: Conduct an Insurance Coverage Check-Up With Your Agent or Insurer

Once you understand the basics of your policy, the next step is confirming whether your coverage still reflects your current needs.

Homeowners often renew policies year after year without reviewing key limits, deductibles, or exclusions. You should schedule a policy review with your insurance agent or carrier and discuss:

- Whether your dwelling coverage reflects current rebuilding costs

- The amount and application of hurricane, wind, and named-storm deductibles

- Whether flood coverage is in place and what limitations may apply

- Any exclusions or endorsements that could affect hurricane-related damage claims

- Recent property improvements that may warrant coverage updates

This conversation can help identify potential coverage gaps before hurricane season begins. Addressing questions early can reduce the risk of underinsurance, claim disputes, and unexpected coverage issues after a storm.

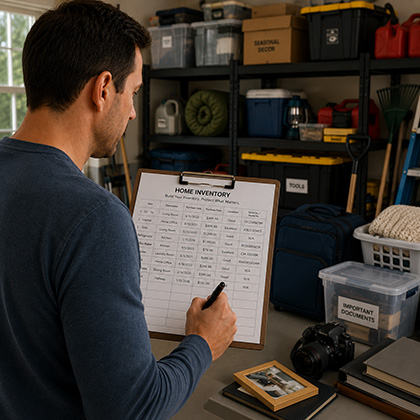

Step 3: Build a Home Inventory That Holds Up During Insurance Disputes

After reviewing your coverage, focus on documenting what you own. A well-organized inventory can make it easier to verify losses and support your claim if hurricane damage occurs.

The 30-Minute Video Inventory (Fast Protection Layer)

A simple video walkthrough provides a strong starting point. Walk through your home, room by room, while recording on your phone. As you record:

- Capture entire rooms, not just valuable belongings.

- Describe major items, including brand and model information when visible.

- Mention approximate purchase dates or values if known.

- Enable date and time settings so metadata is preserved.

This process creates a visual snapshot of your property’s condition and contents before a storm.

The Detailed Inventory (High-Value Homes)

For homes with significant personal property, a more detailed inventory may provide additional protection. Maintain a spreadsheet that includes:

- Item description

- Brand, model, and serial number

- Purchase date

- Original purchase cost

- Estimated replacement value

Whenever possible, attach receipts, invoices, or email purchase confirmations. Photograph serial numbers on appliances, HVAC equipment, and electronics. If documenting vehicles or other high-value assets, include photos showing their location on the property for context.

Storage Strategy That Prevents Claim Failure

Documentation only helps if you can access it after a disaster. Physical-only records can be lost, damaged, or inaccessible after a hurricane.

Store inventory records in secure cloud platforms such as Google Drive, iCloud, or Dropbox. For additional protection, email copies to a trusted out-of-state family member or contact. Keeping timestamped digital records in multiple locations helps preserve evidence and ensures critical information remains available when you need it most.

Step 4: Document Your Home’s “Baseline Condition” Before Hurricane Damage Exists

While a home inventory shows what you own, baseline property documentation shows what condition your home was in before a storm. This step can be especially valuable if questions arise about whether damage resulted from the hurricane or from pre-existing wear and tear.

Create a thorough visual record of your property, including:

- All four sides of the home

- Roofline photos taken from a safe vantage point

- Windows and doors

- Fences, sheds, and other detached structures

- Interior walls, ceilings, and flooring

- Attic areas, if safely accessible

- Electrical panels and other major systems

Store these photos and videos in the same location as your inventory records. If a hurricane damages your property, clear pre-storm documentation can help distinguish storm-related damage from pre-existing conditions. This is one of the most overlooked yet effective steps in understanding what to do before a hurricane.

Step 5: Secure All Insurance Documents in a “Post-Disaster Accessible” Format

Even the best coverage and documentation can create problems if important records become inaccessible after a hurricane. Create a digital archive that includes:

- Homeowners and flood insurance policies

- Declarations pages

- Policy numbers

- Insurance company contact information

- Claims hotline numbers

- Inspection reports

- Appraisal documents

Store login credentials in a secure password manager rather than relying solely on paper records. If you carry flood insurance through the National Flood Insurance Program (NFIP), keep relevant policy information readily available as well.

A dual-storage approach works best. Maintain cloud backups while also keeping copies in a waterproof folder. If internet access becomes limited or devices are damaged, having both options can make recovery easier.

Step 6: Establish Claim Communication Readiness

Communication challenges often arise after a hurricane, especially when local infrastructure experiences outages or disruptions. Preparing for these situations can help you stay connected with your insurer and maintain organized records throughout the claims process.

Before hurricane season, consider:

- Saving insurer contact information in multiple locations

- Keeping written copies of policy numbers

- Recording claim hotline information

- Designating an out-of-area contact who can help relay information if local communication networks are unavailable

- Creating a dedicated folder for future claim-related correspondence

This step is not about emergency response planning. It is about ensuring you can communicate effectively with your insurer and access important information when claim-related issues arise after a storm.

Step 7: Take Protective Measures That Also Strengthen Your Insurance Claim

Protecting your property before a hurricane serves two purposes. It can help reduce the extent of damage and demonstrate reasonable efforts to prevent avoidable losses.

Most insurance policies require property owners to take reasonable steps to protect their property from further damage when possible. Before a storm arrives, consider:

- Trimming trees and removing weak branches

- Cleaning gutters and drainage systems

- Securing outdoor furniture and loose objects

- Installing storm shutters

- Boarding vulnerable windows when appropriate

- Addressing minor maintenance issues that could worsen during severe weather

Document these efforts with dated photographs and videos. If questions arise later, this documentation can help show the condition of your property and the steps taken to prepare for the storm. While taking preventive measures will not eliminate hurricane risk, it can help strengthen your documentation and reduce avoidable complications during the claims process.

What Louisiana and Texas Law Gives You Before You Even File a Claim

Understanding your policy is important, but so is knowing the legal protections available in your state. Louisiana and Texas both have laws designed to promote fair claim handling and provide homeowners with important rights when dealing with hurricane-related property damage claims.

Louisiana Policyholder Rights

Louisiana homeowners may benefit from several legal protections, including:

- Valued Policy Law protections, which affect how certain covered total-loss claims are evaluated under state law.

- Hurricane deductible disclosure requirements, which help ensure policyholders receive clear information about how hurricane or named-storm deductibles apply to their coverage.

- Good-faith claim handling requirements, which generally require insurers to investigate and evaluate claims fairly.

- Timely claim processing and payment obligations, which require insurers to act within 30 days after receiving satisfactory proof of loss. This timeline may be extended to 60 days for catastrophic residential property losses.

These protections help promote transparency and accountability throughout the claims process.

Texas Policyholder Rights

Texas law also provides important safeguards for homeowners after a hurricane or severe storm.

- Prompt Payment of Claims requirements (Chapter 542) generally require insurers to acknowledge a claim within 15 days and, after receiving all requested information, investigate the claim and issue a coverage decision within 15 days. If approved, payment is generally required within five business days. Insurers may receive a 15-day extension in the event of a weather-related catastrophe.

- Pre-suit notice requirements (Chapter 542A) give both parties an opportunity to evaluate and potentially resolve disputes before litigation begins.

- Fair claim handling standards require insurers to reasonably investigate and assess claims.

Knowing these rights before a loss occurs can help homeowners better understand the claims process and recognize potential issues if a dispute arises later.

When to Involve a Hurricane Insurance Lawyer Before the Storm Arrives

Most homeowners do not need legal assistance simply because hurricane season is approaching. However, certain situations may warrant a pre-storm policy review by a property damage attorney. You should consider seeking legal guidance if you have concerns such as:

- Prior claim denials or coverage disputes

- A recent non-renewal notice

- Questions about whether your dwelling coverage limits are adequate

- Uncertainty about flood insurance requirements or flood zone classifications

- Potential gaps between wind and flood coverage

These issues can become significantly more difficult to address once a storm is imminent and coverage changes are restricted.

An attorney can help identify policy language that may create challenges after a hurricane, explain how different coverages interact, and highlight areas that may require further clarification from your insurer. This can be particularly important when a property faces multiple risks, such as wind and flooding, because different types of damage may fall under different policies or coverage provisions.

Early legal review can help homeowners better understand their coverage before a loss occurs. If a claim dispute later develops, having a clear understanding of your policy can put you in a stronger position to evaluate your legal options.

Conclusion

When preparing for hurricane season, protecting your property involves more than stocking supplies and securing your home. Reviewing your insurance coverage, creating a home inventory, documenting your property’s condition, securing important records, taking preventive measures, and planning for claim communications can all help support a smoother claims process if hurricane damage occurs.

Many homeowners focus on what happens after a storm, but insurance challenges often begin long before landfall. Coverage gaps, missing documentation, and policy misunderstandings can create complications when it is time to file a claim. Taking proactive steps now can help you better understand your coverage and strengthen your position if a dispute arises later.

If you have questions about your hurricane coverage, concerns about potential policy gaps, or a history of claim-related issues, speaking with a property damage attorney before hurricane season can provide valuable clarity. Contact Pandit Law for a free case evaluation and guidance on protecting your rights before and after a storm.