A hailstorm can leave homeowners dealing with far more than a few dents on the roof. In many cases, the real frustration begins after the storm passes. Leaks may appear weeks later, hidden roof damage can worsen over time, and insurance companies may dispute whether the damage came from hail, older roofing materials, or normal wear and tear. For many property owners, hail storm damage insurance claims quickly become stressful, confusing, and difficult to navigate alone.

Hail damage is not always easy to spot immediately. Strong winds and hail can damage roofing systems, siding, windows, gutters, and other parts of the home without immediately visible signs. This guide explains what homeowners in Texas and Louisiana should know about identifying hail damage, understanding coverage disputes, and seeking legal guidance when insurance claim problems arise.

What Does Homeowners Insurance Cover for Hail Damage?

Homeowners insurance policies often cover hail-related property damage, but coverage details can vary significantly from one policy to another. Understanding what your policy includes, excludes, and limits can help you avoid surprises during the claims process.

Types of Hail Damage Typically Covered

Most homeowners insurance policies cover sudden storm-related damage caused by hail and wind. Covered damage may include:

- Roof damage from cracked, lifted, or missing shingles

- Siding, gutter, and flashing damage

- Broken windows or skylights

- Interior water damage caused by storm-created openings

- Damage to garages, fences, or other covered structures

Louisiana homeowners need to review any roof schedule endorsements or depreciation provisions in their policies. Some newer policies may limit roof replacement coverage based on the roof’s age or condition following hail and windstorms.

What Insurance Companies May Exclude

Even when a policy covers hail damage, insurers may still dispute portions of the claim. Common exclusions or limitations can involve:

- Wear and tear or aging roof materials

- Pre-existing property damage

- Cosmetic-only damage classifications

- Improper maintenance allegations

Insurance companies may also argue that dents, granule loss, or metal surface damage do not affect the roof’s functionality, which can reduce coverage under a hail storm insurance claim.

Understanding Wind and Hail Deductibles

Many Texas and Louisiana policies include separate wind and hail deductibles. Instead of a fixed dollar amount, these deductibles often use a percentage of the home’s insured value.

For example, a 2% deductible on a $400,000 home may leave the homeowner responsible for $8,000 before insurance coverage applies. In a hail wind damage insurance claim, higher deductibles can significantly affect the final settlement amount.

Actual Cash Value vs. Replacement Cost Coverage

The type of coverage in your policy can significantly affect how insurance companies calculate hail damage payments. Homeowners commonly encounter two types of coverage during the claims process: actual cash value and replacement cost value.

| Coverage Type | How It Works |

| Actual Cash Value (ACV) | Pays the depreciated value of damaged property based on age and condition |

| Replacement Cost Value (RCV) | Pays the cost to repair or replace covered damage, subject to policy terms |

Before moving forward with a claim, homeowners should carefully review their policy language and understand how deductibles, exclusions, and roof coverage limitations can affect recovery after a hailstorm.

Common Signs of Hail Damage Homeowners Should Look For

Hail damage is not always obvious immediately after a storm. Some problems appear right away, while others develop slowly as water enters damaged areas of the home. Identifying damage early can help homeowners protect their property and strengthen a hail wind damage insurance claim.

After a hailstorm, homeowners should look for signs such as:

- Cracked, bruised, lifted, or missing roof shingles

- Dents or cracks in siding and exterior surfaces

- Damage to gutters, flashing, vents, and metal components

- Broken windows, chipped skylights, or damaged window seals

- Water stains on ceilings or walls caused by roof leaks

- Fallen tree limbs, debris impact, or damaged fencing and structures

Homeowners should also inspect for damage caused by neighboring trees, detached structures, or debris blown from nearby properties during the storm. In many cases, homeowners can first file through their own insurance policy rather than pursuing the neighbor directly. If another property contributed to the damage, the insurance company may later seek reimbursement from the responsible party’s insurer through subrogation.

How to File a Hail Storm Damage Insurance Claim for Your Home

Filing hail storm damage insurance claims can feel overwhelming, especially when homeowners discover hidden damage days or weeks after the storm. Taking the right steps early can help protect your property, preserve evidence, and reduce disputes during the insurance process.

Step 1: Stay Safe and Assess the Hail Damage

After a hailstorm, safety should come first. Homeowners should avoid climbing onto roofs or entering unstable areas until the property can be safely inspected.

Common signs of hail damage to look out for include:

- Missing or cracked shingles

- Dented gutters, flashing, or siding

- Broken windows or skylights

- Roof leaks or ceiling stains

- HVAC unit damage

- Fallen trees and debris impact

Step 2: Review Your Homeowners Insurance Policy Before Filing

Before starting a claim, homeowners should review key policy provisions carefully. Understanding coverage limits early may help avoid confusion later.

Important policy terms often include:

- Wind and hail deductibles

- Filing notice requirements

- Actual cash value versus replacement cost coverage

- Cosmetic damage exclusions

- Roof endorsements and depreciation provisions

Some Louisiana policies may also include roof schedule limitations that can affect roof replacement coverage depending on the roof’s age and condition.

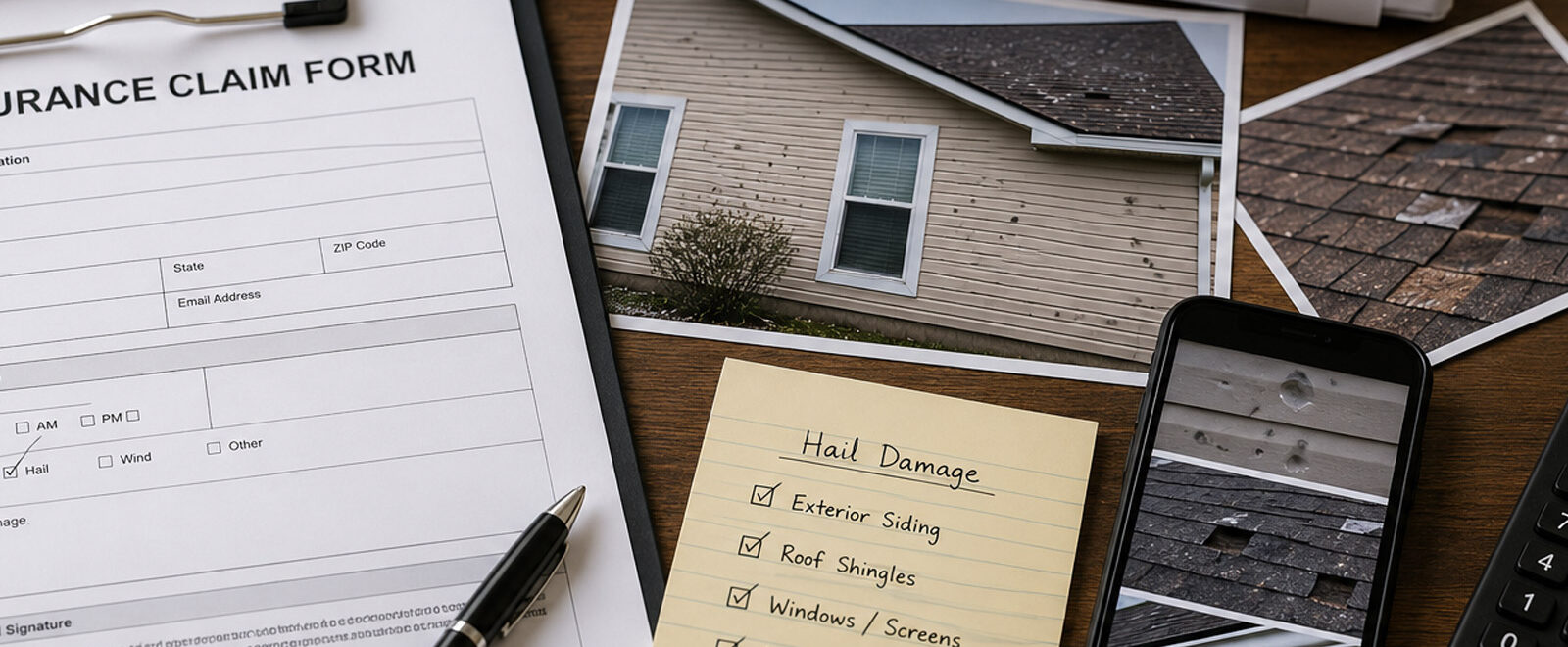

Step 3: Document All Hail Damage Thoroughly

Strong documentation can play an important role in hail storm damage insurance claims. Homeowners should start gathering evidence before major repairs begin whenever possible.

Helpful documentation may include:

- Timestamped photos and videos

- Roof, siding, and gutter damage images

- Interior leaks and water stains

- Fallen trees or debris damage

- Temporary repair invoices

- Contractor estimates and receipts

Step 4: Take Temporary Steps to Prevent Further Damage

Homeowners generally have a responsibility to prevent additional property damage after a storm. Temporary protective measures can help limit worsening conditions while the claim remains under review.

These steps may include:

- Placing tarps over damaged roofing

- Boarding broken windows

- Removing standing water

- Moving damaged belongings away from leaks

Homeowners should keep receipts for temporary repairs and emergency services.

Step 5: Schedule an Independent Hail Damage Inspection

Not all hail damage is immediately visible from the ground. Independent inspections can help identify less visible storm-related damage involving roofing materials, flashing, siding, or structural components that initial evaluations often overlook.

An independent inspection may also help homeowners better understand the full scope of storm-related damage before discussing repairs or settlement estimates.

Step 6: Notify the Insurance Company and Start the Claim

Homeowners should report hail damage promptly after discovering potential storm-related losses. Delays can sometimes lead to disputes about when the damage occurred or whether conditions worsened over time.

Insurance companies commonly request:

- The date of the storm

- Photos of the damage

- A description of affected areas

- Repair estimates or inspection reports

Step 7: Prepare for the Insurance Inspection Process

During the inspection process, the insurance adjuster will evaluate the reported damage and prepare an estimate. Homeowners should carefully review the inspection findings and ask questions if areas appear missing or incomplete.

Common issues leading to disputes in hail storm damage insurance claims include:

- Cosmetic-only damage classifications

- Missed roof or flashing damage

- Low repair estimates

- Partial repair recommendations

Step 8: Review the Insurance Settlement Offer Carefully

Policyholders should closely review settlement offers before beginning repairs or accepting payments. Some estimates may not fully account for all covered storm damage.

Underpayment disputes often involve:

- Excessive depreciation

- Missing repair line items

- Incomplete roofing repairs

- Partial roof replacement disagreements

Step 9: Keep Records of All Claim Communications and Repairs

Organized claim records can help homeowners track the progress of the claim and respond to disputes more effectively.

Important documents to keep include:

- Emails and letters

- Claim numbers

- Inspection reports

- Contractor estimates

- Repair invoices and receipts

Step 10: Contact a Hail Damage Insurance Claim Lawyer if Problems Arise

Homeowners should consider speaking with a property damage attorney if their claim becomes delayed, denied, or underpaid. Legal guidance can help homeowners better understand policy language, disputed damage findings, and settlement disagreements.

An experienced hail damage lawyer can also assist with roof replacement disputes, insufficient settlement offers, or potential bad faith insurance conduct.

Careful documentation, timely reporting, and a clear understanding of policy terms can make a significant difference during the claims process. When disputes arise, homeowners may benefit from experienced legal guidance to protect their rights and pursue coverage for storm-related property damage.

Why Hail Storm Damage Insurance Claims Are Often Denied or Underpaid

Many homeowners expect their insurance policy to cover storm-related losses, only to face delays, reduced estimates, or denied coverage. Hail storm insurance claim disputes often arise when insurers question the cause, extent, or value of the reported damage.

Insurance companies may deny or underpay claims for several reasons, including:

- Wear and Tear Allegations: Insurers sometimes argue that roof damage resulted from aging materials rather than a recent hailstorm.

- Cosmetic Damage Disputes: Dents, granule loss, or metal damage may be classified as cosmetic instead of functional damage.

- Delayed Reporting Claims: Insurers may argue the homeowner waited too long to report the loss, making it harder to verify storm-related damage.

- Incomplete Inspections: Initial inspections may overlook hidden roof, flashing, siding, or water intrusion damage.

- Low Repair Estimates: Some settlement offers may omit labor, materials, code upgrades, or full replacement needs.

- Partial Roof Replacement Disputes: Homeowners often face disagreements involving discontinued shingles, mismatched repairs, or partial replacement recommendations.

In some situations, homeowners may also encounter repeated delays, unclear explanations, or unfair claim handling practices.

When denied or underpaid hail damage claims become difficult to resolve, homeowners may benefit from speaking with a property damage attorney to better understand their rights and available legal options.

Hail Damage Insurance Claims in Louisiana and Texas

Hail and windstorms frequently cause major property damage across Louisiana and Texas. However, claim handling issues, policy limitations, and regional weather risks can affect how homeowners insurance companies evaluate storm-related losses.

Louisiana Hail and Windstorm Insurance Claims

In Louisiana, hail damage often overlaps with hurricane, tropical storm, and wind-driven rain claims. Homeowners in areas such as New Orleans, Baton Rouge, Lake Charles, and other Gulf Coast communities may experience combined roof, siding, and water intrusion damage after severe storms.

Louisiana homeowners need to pay close attention to roof endorsements, percentage deductibles, and depreciation provisions in their policies. Some updated policies may limit roof replacement coverage depending on the roof’s age or condition. Recent Louisiana roofing law changes have also increased requirements for insurance-funded roof replacement work.

Louisiana insurers generally must begin adjusting claims within 14 days after receiving notice of the loss and pay approved claims within statutory deadlines when sufficient proof of loss exists. Homeowners facing delayed, disputed, or underpaid claims may consider speaking with a Louisiana hail damage insurance claim lawyer to better understand their rights and policy obligations.

Texas Hail Damage Insurance Claims

Texas experiences some of the highest rates of severe hailstorms in the country, particularly in areas such as Dallas-Fort Worth, San Antonio, Austin, Houston, and Central Texas. As a result, homeowners frequently deal with roof damage disputes, siding claims, and water intrusion issues after major storms.

Texas hail claims often involve:

- Percentage-based wind and hail deductibles

- Cosmetic damage exclusions

- Aging roof disputes

- Delayed reporting allegations

- Partial roof replacement disagreements

Texas law imposes strict deadlines for acknowledging, investigating, and responding to property damage claims after insurers receive notice and supporting documentation. Prompt inspections, detailed documentation, and early reporting may help homeowners avoid disputes over storm-related damage.

When claim problems arise, a Texas hail damage insurance claim attorney can help homeowners evaluate denied or underpaid storm damage claims and address settlement disagreements.

Storm-related property damage claims can become especially complicated when policies contain roof limitations, cosmetic exclusions, or high deductibles. Understanding state-specific insurance rules and documenting damage carefully can help homeowners better protect their claims.

When to Dispute a Hail Damage Insurance Settlement

Not every settlement offer fully reflects the actual cost of repairing storm-related property damage. Homeowners should review insurance estimates carefully before agreeing to repairs or accepting final payments.

Signs Your Claim May Be Underpaid

Certain issues may indicate the insurance company undervalued the claim, including:

- Repair estimates significantly below contractor pricing

- Missing damage line items

- Denied roof replacement recommendations

- Excessive depreciation deductions

- Incomplete siding or gutter repairs

What to Do if Your Claim Is Denied

If their claim is denied, homeowners should carefully review the denial letter and request a written explanation of the policy provisions involved. It may also help to:

- Preserve photos, videos, and inspection reports

- Obtain additional roofing or property inspections

- Compare contractor findings with the insurer’s estimate

- Keep records of all communications

Appealing a Hail Damage Claim Decision

Homeowners may have options to challenge a denied or underpaid claim through internal appeals, supplemental claims, or other dispute resolution processes available under the policy.

If disagreements continue after additional inspections or documentation, homeowners can benefit from legal guidance before accepting an insufficient settlement.

How a Hail Damage Lawyer Can Help

Hail damage disputes often involve complex policy language, conflicting inspections, and disagreements over repair costs. A hail damage lawyer can help homeowners better understand their rights and address problems involving denied, delayed, or underpaid claims.

Depending on the situation, legal assistance may involve:

- Reviewing denied or underpaid claims

- Identifying potential bad-faith insurance practices

- Handling roof repair and material matching disputes

- Negotiating with the insurance company

- Strengthening claim documentation and evidence

- Addressing hidden or long-term storm damage

- Assisting with supplemental or reopened claims

- Explaining policy obligations and coverage issues

Legal guidance may become especially important when insurers dispute the cause of damage, classify repairs as cosmetic, or recommend partial repairs that fail to address the full extent of the storm damage.

Homeowners do not always realize the extent of hail damage until problems continue to worsen over time. Understanding policy rights, documenting damage carefully, and seeking experienced legal support when disputes arise can help them protect their property and financial recovery after severe storms.

Conclusion

Hail damage can quickly turn into a much larger problem when hidden roof issues, water intrusion, or claim disputes go unaddressed. Acting quickly after a storm, documenting all visible damage, and obtaining thorough inspections can help homeowners protect both their property and their insurance claim rights.

Unfortunately, not all hail storm damage insurance claims are handled fairly. Delays, low settlement offers, and disputed roof damage can create additional stress during an already difficult situation. Homeowners in Texas and Louisiana facing serious claim disputes or insufficient settlement offers may benefit from speaking with an experienced property damage attorney to better understand their legal options and protect their financial recovery after a severe storm.

If you are struggling with a denied or underpaid hail damage claim, Pandit Law can review your situation and help you understand the next steps available under your policy.