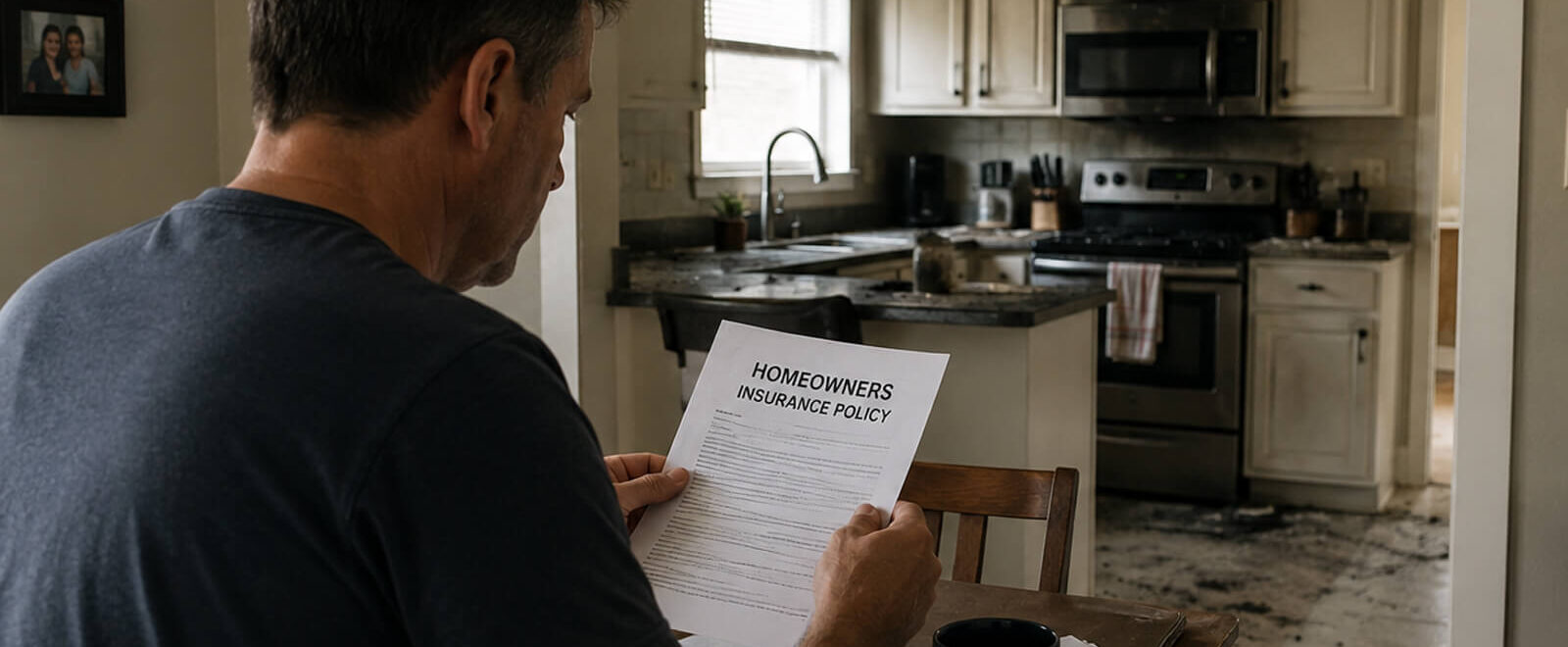

House fires remain one of the most financially devastating events a homeowner can face. Beyond the immediate shock and displacement, fire losses often trigger a second crisis: navigating the details of insurance coverage while trying to rebuild both a home and a sense of stability. In the Gulf South, particularly Louisiana and Texas, this challenge is intensified by older housing stock, extreme weather events, and complex insurance regulations.

Many homeowners assume the answer to the question “Does home insurance cover fire?” is a simple yes. In reality, while most policies include fire as a named peril, the scope of coverage, exclusions, and payout mechanics vary far more than policyholders expect. What’s covered, what’s limited, and what’s excluded outright can significantly affect how much recovery is possible and how long it takes.

This guide helps you understand homeowners insurance fire coverage practically. It explains what policies typically include, where insurers often draw the line, how hidden fire-related damage complicates claims, and why state-specific rules in Louisiana and Texas matter. By the end, you’ll have a clearer understanding of how these details directly shape your fire insurance claim process and your financial recovery.

Understanding Homeowners Insurance Fire Coverage

At its core, homeowners insurance fire coverage is designed to protect against accidental fire losses that damage your home, your belongings, and your ability to live safely in the property. Fire is generally listed as a named peril, which means that coverage applies unless a specific exclusion overrides it.

That said, coverage is never unlimited. Every fire insurance claim is subject to policy limits, deductibles, sub-limits for certain property types, and conditions that govern how losses must be documented. Even when fire coverage exists, disputes often arise over valuation, scope of necessary repairs, and whether related damage truly resulted from the fire event or from a pre-existing issue.

Understanding how these coverage elements work together allows homeowners to document losses with purpose, anticipate insurer objections, and avoid gaps that lead to underpayment. When coverage is challenged, this knowledge helps homeowners assess whether the policy is being applied fairly or strategically narrowed to limit payout. It also helps them respond clearly before the claim stalls or shrinks.

What’s Covered by a Homeowners Policy for a Fire Damage Claim

A standard homeowners policy typically responds broadly to accidental fire losses, covering both direct and secondary damage, including:

- Dwelling and Structural Protection: This generally includes walls, roofs, ceilings, framing, built-in cabinetry, flooring, and permanently installed fixtures damaged by flames, heat, smoke, or water used to extinguish the fire. Even partial structural damage can qualify if repairs are required to restore safety and habitability.

- Other Structures Coverage: Protection often extends to detached garages, sheds, fences, or guest houses affected by the fire. This coverage usually carries a separate limit, expressed as a percentage of the main dwelling coverage.

- Personal Property Coverage: Designed to protect contents inside the home, this coverage includes furniture, clothing, electronics, appliances, and household items. Fire damage claims often involve disputes over depreciation versus replacement cost, particularly for older belongings.

- Additional Living Expenses (ALE) Coverage: ALE helps pay for temporary housing, meals, transportation, and other necessary costs when the home becomes uninhabitable due to fire damage. This coverage is critical after major losses and is often subject to time and dollar limits.

- Smoke and Related Losses: Smoke damage is also typically covered and can extend far beyond the area directly affected by flames, affecting walls, insulation, HVAC systems, and personal property throughout the home.

Most accidental fire causes fall within coverage, provided they are not excluded by policy conditions, including:

- Cooking accidents, which remain the leading cause of residential fires

- Lightning strikes

- Faulty or overloaded electrical wiring

- Candles, fireplaces, or space heaters

- Accidental ignition from routine household activities

What’s Not Covered by a Homeowners Policy for a Fire Damage Claim

While coverage for fire is broad, it is not absolute. Insurers frequently rely on exclusions to limit or deny portions of a fire insurance claim, such as:

- Intentional Acts: Fire caused by arson committed by the homeowner, or someone acting on their behalf, is excluded. Even suspicion of intentional conduct can trigger extensive investigations and delays.

- Maintenance-Related Issues: Insurers may attempt to limit coverage by arguing that deteriorated wiring, neglected appliances, or code violations caused the fire, characterizing the loss as preventable rather than accidental.

- High-Value Items: Expensive belongings, such as jewelry, fine art, collectibles, and firearms, are often subject to sub-limits unless separately scheduled. Fire damage to these items may not be fully reimbursed without additional endorsements.

- High Wildfire Risk Zones: Properties located in designated wildfire risk areas may face special exclusions or non-renewal issues, particularly in certain Texas regions, depending on underwriting rules.

- Vacancy Clauses: Vacancy is a common but often overlooked limitation. Homes left unoccupied for more than 30 consecutive days may lose fire protection entirely unless specific coverage is maintained.

These exclusions not only affect coverage but also influence how insurers investigate fire damage claims and whether disputes arise over cause, responsibility, or scope of losses.

The Hidden Fire Damages: Are They Covered by Your Home Insurance?

Fire losses are rarely limited to what’s visible after the flames are extinguished. Some of the most expensive and dangerous consequences often surface later, during inspections or repairs. Whether these hidden damages are covered depends on policy language, how losses are documented, and how the claim is presented.

- Thermal Bridging and Structural Fragility: Extreme heat can weaken wood framing, steel supports, fasteners, and load-bearing connections without leaving obvious charring. Even when materials look intact, heat exposure can reduce their structural integrity, leading to sagging, cracking, or failure months later. These losses are often missed in initial inspections unless properly evaluated and documented.

- Toxic Residue from Modern Building Materials: Many homes today contain plastics, foams, adhesives, and synthetic finishes that release corrosive gases and fine particulate residue when burned. These toxins can penetrate drywall, insulation, cabinetry, and HVAC systems, creating long-term health risks. Effective remediation often requires removal and replacement rather than surface cleaning. Insurers, however, frequently resist acknowledging this broader scope of damages.

- Smoke and Soot Contamination Beyond the Fire Area: Smoke travels far beyond the room where the fire started, spreading through wall cavities, ceilings, and ventilation systems. Soot particles embed into porous materials, causing persistent odors and respiratory concerns. Smoke-only damage is commonly minimized by insurers, even though it often requires specialized testing, deodorization, or material replacement.

- Water Damage and Mold Growth from Fire Suppression: Water used to extinguish a fire can saturate floors, drywall, substructures, and insulation. If drying is delayed or incomplete, moisture can lead to warping, rot, and mold growth. Insurers may attempt to classify mold as a separate or limited loss unless water damage is clearly tied to firefighting efforts.

- Compromised Electrical Systems: Fire heat can degrade wiring insulation, breakers, outlets, and electrical panels, even if they never ignited. These hidden failures increase the risk of future fires and code violations. Electrical systems exposed to heat often require full replacement rather than spot repairs. This becomes an issue that insurers frequently dispute without a thorough evaluation.

Key Considerations for Comprehensive Fire Damage Coverage

Fire claims often expose gaps in coverage that homeowners never realized existed. Understanding how policy mechanics operate, both before and after a loss, can make the difference between a smooth recovery and a financially draining dispute.

Coverage limits must reflect real rebuilding costs, not market value

After a fire, insurers pay to repair or rebuild the structure, not to match the home’s pre-loss market value. Construction costs, labor shortages, and material inflation can push rebuilding expenses far beyond policy limits, leaving underinsured homeowners responsible for the shortfall.

Deductibles directly impact how much recovery actually reaches you

Fire deductibles apply before any payment is issued and can significantly reduce claim proceeds, especially for partial losses. Homeowners often underestimate how deductibles affect cash flow during repairs, when upfront funds are needed most.

Building code upgrades can become a major uncovered expense

Fire repairs frequently trigger code compliance requirements, such as updated electrical systems, fire-resistant materials, or safety installations. Most standard policies exclude these costs unless ordinance or law coverage is in place, shifting thousands of dollars in mandatory upgrades onto the homeowner.

Policy language determines whether hidden fire damage is fully addressed

Limits on smoke, water, mold, or toxic residue remediation are often buried deep in policy endorsements. These restrictions commonly surface only after a claim is filed, when insurers narrow the scope of repairs based on technical exclusions rather than the full extent of damages.

Proactive policy review strengthens claim leverage before disputes arise

Homeowners who understand their coverage structure are better positioned to challenge underpayment, push back against exclusions, and present claims that reflect the full extent of fire-related loss, which is not just what is immediately visible.

How Fire Damage Coverage Differs in Louisiana and Texas

Fire claims are governed not just by policy language, but by state-specific laws that affect timelines, penalties, and claim-handling obligations.

Navigating Fire Coverage in Louisiana

Louisiana regulates fire coverage under the Standard Fire Insurance Policy framework (RS 22:1311), which establishes baseline protections for policyholders and influences how fire losses are valued. In cases of total loss, Louisiana law (RS 22:1318) generally bases insurer liability on the insured’s interest in the property, though partial losses may be treated differently. Policyholders may also be entitled to advance payments for Additional Living Expenses, often covering at least four months after a total loss.

Navigating Fire Coverage in Texas

Texas fire claims are governed by the Texas Insurance Code and the Prompt Payment of Claims Act (§ 542). Insurers must meet strict deadlines:

- Acknowledge receipt within 15 days

- Accept or deny the claim within 15 days after receiving the required information

- Issue payment within 5 business days of acceptance

Failure to comply can result in annual interest and potential attorney’s fees.

Texas law also mandates an appraisal provision under SB 458 (Chapter 1813) for all residential policies issued or renewed after January 1, 2026. While the appraisal resolves the amount of loss and is generally binding, it does not address coverage disputes or causation issues, which often require legal intervention when disagreements arise.

How a Lawyer Can Help You After Fire Damage

Fire damage claims often become adversarial once insurers begin questioning the scope of loss, valuation, or cause of the fire. Legal guidance helps level the playing field when insurers narrow coverage or stall payment on a fire damage claim.

A lawyer can assist by:

- Reviewing Policy Language and Coverage Triggers: A lawyer analyzes how your policy defines covered fire losses, exclusions, endorsements, and conditions, identifying where coverage should apply and where insurers may be misinterpreting or narrowing the contract.

- Ensuring Claims Are Properly Filed and Documented: Legal guidance helps structure the claim from the outset, aligning documentation, timelines, and damage categories so insurers cannot later challenge the claim on technical or procedural grounds.

- Identifying Improper Exclusions or Undervaluation: Attorneys spot when insurers rely on exclusions that don’t fit the facts or use pricing assumptions, depreciation, or partial repairs to undervalue legitimate fire-related losses.

- Negotiating Disputes Over Scope, Repairs, and ALE: When insurers limit repairs or reduce ALE coverage, a lawyer pushes back with evidence-based arguments that reflect actual restoration needs and displacement realities.

- Challenging Wrongful Denials or Delays: Legal intervention addresses unjustified denials or prolonged “investigations” by enforcing policy obligations and, when necessary, escalating the dispute beyond adjuster-level review.

- Applying State-Specific Laws in Louisiana and Texas: Fire claims are governed by strict state statutes. Lawyers use Louisiana and Texas insurance laws, deadlines, and penalty provisions to hold insurers accountable and strengthen recovery.

Conclusion

So, does home insurance cover fire? In most cases, yes, but the outcome depends on policy language, exclusions, documentation, and state law. Homeowners insurance fire coverage can protect against devastating losses, but only when claims are handled carefully and disputes are addressed early.

Understanding what’s covered, what’s excluded, and how insurers evaluate fire damage puts homeowners in a stronger position. When coverage becomes contested, legal advocacy can make the difference between partial recovery and full restoration.

If your fire damage claim is delayed, underpaid, or denied, consider seeking a FREE Claim Evaluation to better understand your rights and options.

Frequently Asked Questions

Coverage generally applies only if the homeowner did not intentionally cause the fire. Because arson allegations raise fraud concerns, insurers investigate these claims closely and aggressively, which can delay resolution even when coverage ultimately applies.

Start by ensuring everyone’s safety and securing temporary housing. As soon as possible, document all losses, notify your insurer, and keep records of expenses, as early documentation plays a critical role in how the claim is evaluated. Consider seeking legal guidance early in the process to ensure your rights as a policyholder are protected.

Homeowners liability coverage may apply if you’re found legally responsible for the fire spreading to a neighboring property. These claims often involve fault determinations, making documentation and early legal intervention especially important.

Yes, electrical fires are typically covered when they result from accidental causes, such as faulty wiring or appliance failure. Coverage disputes may arise if insurers argue the fire resulted from long-term maintenance issues or code violations.

Most accidental fires fall within standard policy coverage. However, insurers may still scrutinize how the fire started to determine whether any exclusions apply.

Chimney fires are often covered if they occur suddenly and accidentally. Coverage may be limited or denied if the insurer claims the fire resulted from neglect or lack of maintenance.