Imagine you spend days cleaning up after a tornado tears through your home, only to receive a denial letter from your insurance company weeks later. For many homeowners and business owners across the Gulf Coast, that frustration becomes part of the recovery process during severe Southern storm seasons.

Texas consistently reports some of the highest tornado activity in the country, with 162 tornadoes reported in 2025 alone. Louisiana also averages approximately 60 tornadoes each year. Nationwide, preliminary tornado reports reached more than 1,500 in 2025, well above historical averages.

As tornado-related property damage increases across the South, many homeowners discover that recovering through the insurance process can become another challenge entirely. Homeowners can face denied tornado damage claims for several reasons, including disputes over roof damage, pre-existing conditions, policy exclusions, or undervalued inspections. Understanding the insurer’s tactics and the exact reason behind the denial can help them better challenge the decision and protect their claim.

Reasons Tornado Damage Claims Get Denied

After a major storm, many homeowners expect their insurance coverage to help them rebuild and move forward. Instead, they may face delays, reduced payments, or a tornado insurance claim denial that leaves them struggling to recover.

Insurance companies may deny or undervalue claims for several reasons, especially when disputes arise over the source, extent, or timing of the damage, such as:

Insurance Company Claims the Damage Was Pre-Existing

One of the most common reasons why insurance companies deny tornado claims involves allegations that the damage already existed before the storm. Insurers may argue that roof deterioration, cracked shingles, or structural issues developed over time rather than during the tornado itself.

These disputes often involve:

- Aging roofs nearing the end of their expected lifespan

- Previous hail, wind, or storm damage

- Wear and tear exclusions in the policy

- Prior repair issues or unresolved property damage

In some cases, the insurance company may rely on older inspection reports, satellite images, or limited inspections to support its position. Homeowners often discover that proving when the damage occurred becomes a major part of challenging the denial.

Insurer Blames Flooding Instead of Wind Damage

Tornadoes often bring heavy rain, storm surge, and flash flooding alongside destructive winds. Because many homeowners insurance policies cover wind damage differently than flood-related losses, insurers may dispute how the damage occurred.

For example, an insurer may claim rising water caused the damage instead of tornado winds. That distinction can significantly affect available coverage and may lead to delayed or denied payments.

These disputes commonly involve:

- Roof openings that allowed water intrusion

- Structural collapse after severe wind events

- Interior water damage following roof damage

- Mixed wind and flood damage affecting the same property

The way damage gets classified can play a major role in whether a claim receives full, partial, or denied coverage.

The Adjuster Undervalued the Damage

Some tornado claims are not denied outright but instead severely underpaid after the inspection process. Adjusters may overlook hidden damage that becomes more visible weeks or months after the storm. This can include:

- Structural shifting or foundation concerns

- Water intrusion behind walls or ceilings

- Electrical system damage

- Damage to insulation or HVAC systems

- Mold growth caused by prolonged moisture exposure

A rushed inspection or incomplete evaluation can result in repair estimates that fail to account for the full scope of the loss. In many situations, homeowners only learn about additional damage after contractors begin repairs.

Policy Exclusions or Technicalities

Insurance companies may also rely on exclusions, coverage limitations, or technical policy language to deny tornado-related losses. Even when tornado damage appears obvious, disputes may arise over what portions of the property qualify for coverage.

Common examples of exclusions include:

- Detached garages, sheds, or fences

- Cosmetic roof damage disputes

- Coverage limitations tied to older roofing systems

- Exclusions involving certain materials or structures

Recent Louisiana homeowners insurance policy changes involving roof schedules and depreciation have also created additional coverage concerns for some property owners. Reviewing the exact policy language often becomes critical after a denial letter arrives.

Documentation or Filing Issues

Missing documentation can create problems during the claims process, particularly after widespread tornado outbreaks when insurers handle large numbers of claims at once. Insurance companies may argue that evidence supporting the reported damage is insufficient.

Important records homeowners must organize include:

- Photos and videos of the property damage

- Contractor repair estimates

- Engineering evaluations

- Temporary repair receipts

- Claim-related emails and letters

Keeping organized records can help homeowners respond more effectively if the insurance claim is denied or questioned later in the process.

Maintenance Issues

Insurance companies sometimes argue that poor property maintenance contributed to the loss. They may claim the tornado worsened existing issues rather than caused the primary damage itself.

These disputes often involve aging roofs, older building materials, or previously neglected repairs. Insurers may also point to maintenance records, prior claims, or inspection findings when attempting to deny your claim.

Understanding the reason behind the denial can help homeowners identify whether the insurance company handled the claim fairly and what options may still be available moving forward.

Bad Faith Insurance Practices After Tornado Damage

Not every denied tornado claim is an example of insurance bad faith. Insurance companies have the right to investigate claims and dispute losses when legitimate coverage questions exist. However, unfair claim-handling practices may violate Texas or Louisiana law when insurers fail to act reasonably, honestly, or in good faith.

Homeowners should watch for potential warning signs during the claims process, including:

- Delaying investigations without a reasonable explanation

- Repeatedly requesting the same documents or information

- Offering settlements that appear far below documented repair estimates

- Misrepresenting policy terms or coverage provisions

- Denying claims without conducting a thorough inspection

- Failing to respond to emails, calls, or claim inquiries

- Assigning multiple adjusters, resulting in inconsistent evaluations

- Providing conflicting reasons for denying the claim

- Issuing payments that do not reflect the full scope of covered damage

These practices can create significant financial and emotional stress for property owners already dealing with tornado-related losses.

The insurer’s conduct during the claims process can sometimes reveal issues that are not obvious from the denial letter alone. If an insurance claim is delayed or denied and the insurer’s conduct appears unreasonable, it may be worth reviewing the claim more closely to determine whether your rights have been affected.

Your Rights Under Texas and Louisiana Bad Faith Insurance Laws

Texas and Louisiana both require insurance companies to handle claims fairly and in good faith. When insurers fail to meet their legal obligations, homeowners may have options to challenge delayed, underpaid, or denied tornado claims.

Louisiana

Louisiana law requires insurers to adjust claims fairly, conduct reasonable investigations, and communicate promptly with policyholders. Insurers generally must acknowledge receipt of a claim within 14 days after receiving notice and, after receiving satisfactory proof of loss, pay the undisputed portion of a covered claim within 30 days. However, following a declared catastrophe or emergency, the Louisiana Legislature or the Louisiana Department of Insurance may temporarily extend certain statutory claim handling deadlines to account for the extraordinary volume of claims. Even when such extensions apply, insurers remain obligated to investigate, communicate, and adjust claims in good faith.

Homeowners may have concerns when insurers:

- Fail to properly investigate tornado damage.

- Ignore evidence supporting the claim.

- Unreasonably delay claim decisions or payment beyond any applicable statutory deadlines.

- Rely on unsupported or insufficient reasons to deny coverage.

When unfair claim handling practices occur, policyholders may have legal remedies under Louisiana law. A Louisiana tornado damage lawyer can review the denial letter, policy language, claim history, and the applicability of any catastrophe-related deadline extensions to determine whether the insurer fulfilled its legal obligations.

Texas

Texas law generally requires insurers to acknowledge receipt of a claim, begin an investigation, and request any reasonably necessary information within 15 days after receiving notice of the claim. After receiving all requested information, insurers generally must accept or reject the claim within 15 business days. If the claim is approved, payment is generally due within 5 business days.

Texas law also permits insurers to extend the claim determination deadline by up to 45 additional days in certain circumstances, provided the insurer notifies the policyholder in writing and explains the reason for the delay. In addition, following a catastrophe, the Texas Department of Insurance may authorize temporary extensions of certain statutory claim handling deadlines to address the extraordinary volume of claims. Even when these extensions apply, insurers remain obligated to investigate, communicate, and handle claims in good faith and within the applicable legal timeframes.

Homeowners have the right to expect:

- Timely communication regarding the status of their claim.

- A thorough and reasonable investigation of tornado damage.

- Clear explanations for coverage decisions.

- A fair evaluation of covered losses.

When delays, denials, or underpayments appear unreasonable, a Texas tornado damage attorney can evaluate whether the insurer complied with the Texas Prompt Payment of Claims Act, any applicable catastrophe-related extensions, and its broader obligations under Texas law.

Understanding these state-specific rights can help homeowners make informed decisions when an insurer’s handling of a tornado damage claim raises concerns.

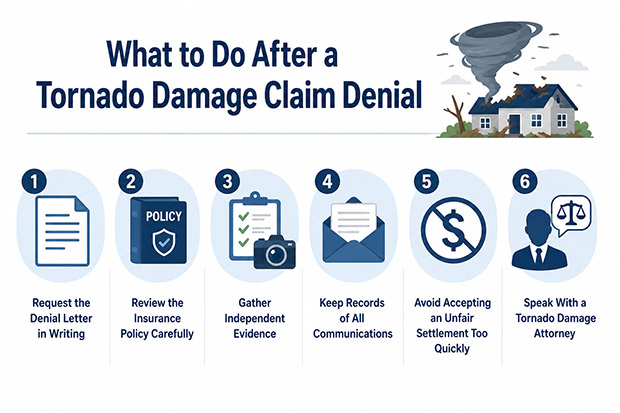

What to Do After a Tornado Damage Claim Denial

Receiving a denial can feel overwhelming, especially when you are already dealing with storm-related repairs and financial uncertainty. However, a denied tornado damage claim is not always the end of the process. Taking the right steps after a denial can help you better understand the insurer’s position and evaluate your available options.

Request the Denial Letter in Writing

If the insurance company denies your claim, request a written denial letter if you have not already received one. The letter should explain the specific reason for the denial and identify any policy provisions the insurer relied upon.

Reviewing the denial letter carefully can help you determine whether the insurer cited a coverage exclusion, disputed the cause of the damage, or claimed insufficient evidence. Understanding the exact basis for the decision is often the first step toward responding effectively.

Review the Insurance Policy Carefully

After receiving the denial letter, compare the insurer’s explanation with your policy language. Policy terms can be complex, and coverage disputes often arise from differing interpretations of specific provisions.

Pay close attention to:

- Coverage exclusions

- Deductible requirements

- Policy endorsements or amendments

- Definitions related to wind, storm, or tornado damage

- Coverage limitations affecting certain structures or property components

A careful review can help reveal whether the denial aligns with the policy or whether additional questions need to be addressed.

Gather Independent Evidence

Insurance companies rely on their own inspections and evaluations when making claim decisions. If you disagree with the denial, gathering independent evidence can help support your position.

Useful documentation may include:

- Contractor repair estimates

- Engineering reports

- Photos and videos of the damage

- Weather reports and storm data

- Repair invoices and receipts

- Temporary mitigation records

Strong documentation can help clarify the cause, extent, and timing of the damage, particularly when the insurer claims the loss resulted from pre-existing conditions or uncovered causes.

Keep Records of All Communications

Good recordkeeping becomes especially important when dealing with denied tornado damage claims. Miscommunications, missing information, or conflicting explanations can complicate an already difficult process.

Consider maintaining copies of:

- Emails with the insurance company

- Written correspondence

- Claim status updates

- Inspection reports

- Notes from phone conversations, including dates and names of representatives

A detailed record can help establish a timeline of events and provide valuable context if disputes arise later.

Avoid Accepting an Unfair Settlement Too Quickly

Sometimes an insurer may offer a payment after initially questioning or partially denying a claim. While receiving funds may seem like progress, it is important to understand what the payment covers before accepting it.

A quick settlement may not fully account for hidden structural damage, ongoing water intrusion issues, electrical system damage, or other losses that become apparent over time. Taking time to evaluate the scope of the damage can help homeowners make more informed decisions.

Speak With a Tornado Damage Attorney

When claim disputes become complicated, legal guidance can help homeowners better understand their rights and available options. A tornado damage attorney can review the denial letter, insurance policy, claim documentation, and communications with the insurer.

Depending on the circumstances, an attorney can help identify coverage issues, evaluate whether the claim was handled fairly, and explain potential next steps. This can be particularly valuable when denied tornado damage claims involve substantial property damage or ongoing disagreements with the insurance company.

Taking the right steps early can help preserve important evidence and strengthen your response to the denial. By gathering evidence, reviewing the insurer’s reasoning, and understanding your rights, you can make more informed decisions about how to move forward after a tornado-related claim dispute.

How an Attorney Helps with Denied Tornado Damage Claims

When a tornado claim is denied, homeowners often need to sift through complex policy language, conflicting damage assessments, and ongoing disputes with the insurance company. An attorney can help evaluate the situation and explain the options available based on the specific facts of the claim.

A tornado damage attorney can help you:

- Analyze policy language and the denial reason to identify the basis for the insurer’s decision.

- Gather additional evidence, such as contractor estimates, engineering reports, and damage documentation that may support the claim.

- Handle communications with the insurance company to help ensure concerns and supporting evidence are properly presented.

- Identify potential signs of bad faith insurance practices, including unreasonable delays, inadequate investigations, or inconsistent claim explanations.

- Pursue appeals, negotiations, or legal action when appropriate and supported by the facts.

Every claim is different, and a denial does not automatically mean the insurance company acted improperly. However, a careful review of the policy, claim file, and insurer’s actions can help homeowners better understand their rights and determine whether additional steps may be available after a denied tornado damage claim.

Conclusion

A tornado can damage a property in minutes, but disputes over insurance coverage can continue for months. What many homeowners do not realize is that claim outcomes often depend as much on documentation, inspections, and policy interpretation as they do on the damage itself. As a result, a denial or underpayment does not always reflect the full merits of a claim.

While denied tornado damage claims can create significant financial and emotional stress, homeowners may still have options to challenge unfair denials, disputed damage assessments, or inadequate payments. Understanding the reason behind a tornado insurance claim denial is often the first step toward protecting your rights.

If your tornado claim has been denied, delayed, or underpaid in Texas or Louisiana, contact Pandit Law for a free consultation to discuss your situation and explore your legal options.