When a sudden freeze hits Texas or Louisiana, the damage can happen fast. Homeowners can wake up to a burst pipe, soaked drywall, ruined flooring, and thousands of dollars in water damage. After years of paying insurance premiums, many expect their policy to help cover the loss. Instead, they receive a denial letter.

Unfortunately, frozen pipe insurance claim denials are more common than many homeowners realize. For example, during Winter Storm Uri, frozen and burst pipes led to tens of thousands of insurance claims across Texas as widespread power outages left many properties without heat. Yet insurers often deny claims by arguing the homeowner failed to maintain heat, prevent freezing, or properly maintain the property.

For homeowners already dealing with significant property damage, a denied frozen pipe claim can add another layer of stress and uncertainty. However, a denial is not always final. In some cases, a property damage attorney can review the policy, investigate the denial, and help homeowners challenge unfair claim decisions.

What Your Homeowners Policy Covers (and Doesn’t) for Frozen Pipe Damage

Many homeowners assume any damage caused by a frozen or burst pipe is automatically covered by insurance. In reality, coverage often depends on the cause of the damage, the policy language, and whether the insurer believes reasonable steps were taken to protect the property during cold weather.

What Homeowners Insurance Typically Covers

Most standard homeowners insurance policies cover sudden and accidental damage caused by frozen or burst pipes. Depending on the policy, coverage may include:

- Water damage resulting from a burst pipe

- Repairs to walls, ceilings, flooring, and other damaged structural components

- Damage to personal property caused by water intrusion

- Costs associated with locating and accessing the damaged pipe

- Additional living expenses if the home becomes temporarily uninhabitable due to a covered loss

Coverage generally focuses on the resulting damage rather than the freezing event itself. However, insurers often review the circumstances closely before approving a claim.

What Is Commonly Not Covered

Not every water-related loss qualifies for coverage. Many policies contain exclusions that insurers frequently cite when denying claims.

Common exclusions may include:

- Flood damage from rising water or storm surge

- Gradual leaks that develop over time

- Wear and tear, deterioration, or corrosion

- Maintenance-related issues

- The cost of replacing aging plumbing systems that failed due to normal deterioration

Insurers may also dispute whether the damage resulted from a sudden freeze or a pre-existing condition.

The Key Policy Clause Insurers Rely On

One of the most important provisions in many policies is the “freezing of plumbing” clause. This language often requires homeowners to take reasonable precautions when freezing temperatures are expected.

Insurers commonly rely on this clause to argue that a claim should be denied because the homeowner failed to:

- Maintain heat inside the property

- Shut off the water supply during an extended absence

- Drain plumbing systems when appropriate

As a result, understanding the exact language in your policy can be critical when evaluating whether a frozen pipe claim denial is justified.

The Real Reasons Frozen Pipe Insurance Claims Get Denied

Many homeowners assume that a burst pipe automatically means insurance coverage. Unfortunately, that is not always how insurers evaluate these losses. In many denied frozen pipe insurance claims, the dispute centers on whether the homeowner took reasonable steps to protect the property before and after the freeze.

Understanding the most common denial reasons can help homeowners identify potential problems and better evaluate whether a denial may be challenged.

Lack of Heat or Negligence Allegations

One of the most common reasons insurers deny frozen pipe claims is by arguing that the homeowner failed to maintain adequate heat inside the property. Many denial letters claim the homeowner acted negligently or failed to take reasonable precautions during cold weather.

Insurers often focus on issues such as:

- Failing to maintain adequate heat inside the property

- Failing to monitor the property during a winter storm

- Ignoring weather warnings

- Not taking steps to protect exposed plumbing

These allegations became especially common after Winter Storm Uri in 2021. Millions of Texans lost power during the storm, leaving homes without heat for extended periods. Despite widespread outages in Dallas, Houston, Austin, San Antonio, and Beaumont, many homeowners still faced claim disputes involving allegations that they failed to maintain heat or prevent frozen pipes.

Similar concerns emerged during Winter Storm Fern in 2026, which brought ice, snow, dangerous temperatures, and widespread power outages across Louisiana, including areas near Shreveport, Monroe, and Baton Rouge.

In many denied claims, the central dispute is whether the loss resulted from circumstances outside the homeowner’s control or from alleged negligence.

Understanding the “55-Degree Guideline”

Many homeowners insurance policies require policyholders to take reasonable steps to prevent freeze-related damage. Although policy language varies, maintaining adequate heat inside the home and protecting plumbing systems during freezing conditions can be important factors in determining coverage for frozen pipe claims. Some insurers and property management professionals recommend keeping indoor temperatures at approximately 55°F or higher during cold weather.

When investigating a claim, insurers may review:

- Smart thermostat records

- Utility usage history

- Power consumption data

- Inspection reports

- Statements made during the claim process

If utility records show little or no heat usage during the freeze, insurers may argue that the homeowner failed to protect the property. In some cases, homeowners discover that a thermostat malfunction, power outage, or heating system failure becomes the basis for a denial.

Because these disputes often involve technical evidence, policy language and supporting documentation can play a significant role in determining whether the denial is justified.

Wear and Tear or Poor Maintenance

Another common explanation insurers use involves allegations that the plumbing system was already deteriorating before the freeze occurred.

Insurance companies frequently argue that the pipe failed because of:

- Corrosion

- Aging plumbing materials

- Poor insulation

- Long-term deterioration

- Deferred maintenance

Instead of treating the loss as a sudden freeze event, the insurer may characterize it as a maintenance issue. Pre-existing damage is frequently cited in denial letters because most policies exclude ordinary wear and tear.

This issue often arises in older homes throughout New Orleans neighborhoods such as Lakeview and Mid-City, as well as Baton Rouge, Galveston, and parts of East Texas, where aging pipe infrastructure remains common. In these situations, the dispute often centers on whether the pipe failed because of a sudden freeze event or because the insurer believes deterioration existed long before the cold weather arrived.

Vacancy or Extended Absence

Many homeowners do not realize that vacancy provisions can significantly affect coverage.

Some policies require homeowners to take additional precautions if a property will remain unoccupied for an extended period. Those precautions may include maintaining heat, shutting off the water supply, or draining plumbing lines.

Insurers often scrutinize claims involving:

- Seasonal homes

- Vacation properties

- Second homes

- Extended travel periods

- Unoccupied residences

Many snowbirds in Louisiana and second-home owners throughout East Texas encounter problems when insurers determine the property was vacant during the freeze.

Even when a homeowner believed the property was properly protected, insurers may argue that policy conditions were not satisfied. As a result, vacancy-related provisions frequently appear in frozen pipe insurance claim disputes.

Late Reporting or Documentation Issues

The actions taken immediately after a burst pipe can affect how an insurer evaluates the claim. Insurance companies may question a claim when:

- The damage was reported days or weeks later

- Photos were not taken before cleanup began

- Repair records are incomplete

- Damaged materials were discarded too quickly

Insurers sometimes argue that delayed reporting prevented them from fully investigating the cause of the damage.

Documentation becomes especially important because burst pipe losses often involve extensive water damage that can change significantly during cleanup and repair work. When evidence disappears before inspection, insurers may use that gap to dispute portions of the claim.

Failure to Mitigate Further Damage

Most policies require homeowners to take reasonable steps to prevent additional damage after a pipe bursts. This may include:

- Shutting off the water supply

- Contacting emergency repair services

- Removing standing water when possible

- Protecting undamaged portions of the property

Insurers may partially deny claims if they believe additional damage occurred because reasonable protective measures were delayed. For example, prolonged moisture exposure can increase structural damage and complicate repairs. Insurers sometimes argue that part of the loss could have been avoided if action had been taken sooner.

These disputes often focus on what was realistically possible under the circumstances, particularly during widespread winter emergencies.

Flood vs. Water Damage Disputes

Another reason homeowners find their frozen pipe insurance claim denied involves disputes over the source of the water.

Burst pipe damage is generally treated differently from flood damage under many policies. Because flood-related losses often require separate coverage, insurers may closely examine where the water originated.

These disputes often arise when:

- Flooding and burst pipes occur simultaneously

- Storm conditions affect multiple properties

- Water enters from several sources

- The cause of the damage is unclear

When multiple causes contribute to the damage, determining the true source of the loss often becomes a major point of contention. This issue can be especially significant in coastal Louisiana and low-lying areas of Houston and Harris County, where flooding frequently accompanies severe weather events. In these situations, inspection reports, plumbing evaluations, and weather records often become critical pieces of evidence.

Hidden Policy Exclusions

Many homeowners never read every endorsement or exclusion contained in their policy. However, insurers frequently rely on policy provisions involving:

- Vacancy restrictions

- Freezing-related conditions

- Water damage limitations

- Maintenance obligations

- Certain mold-related limitations

These provisions often appear in denial letters after a loss occurs.

Because policy language can be complex, homeowners sometimes discover important limitations only after receiving a denial. Understanding how these exclusions interact with the facts of the loss is often critical when evaluating a disputed claim.

Insurance Bad Faith Tactics

Not every denial results from a legitimate coverage dispute. In some situations, homeowners believe the insurer handled the claim unfairly from the beginning.

Common indicators of unfair claim handling include:

- Ignoring evidence that supports coverage

- Selectively relying on information that favors denial

- Interpreting ambiguous policy language against the homeowner

- Failing to conduct a reasonable investigation

- Delaying decisions without a reasonable explanation

Homeowners may also encounter situations where the insurer focuses heavily on finding reasons to deny coverage while giving little attention to evidence supporting the claim.

When insurers fail to fairly investigate, evaluate, or communicate regarding a claim, homeowners may begin questioning whether the denial resulted from improper claim handling rather than the actual policy language.

A denied frozen pipe claim does not automatically mean the matter is closed. In some cases, further investigation, documentation, and legal review may reveal that the denial deserves closer scrutiny. Understanding why the frozen pipe insurance claim was denied is often the first step toward determining what options may still be available.

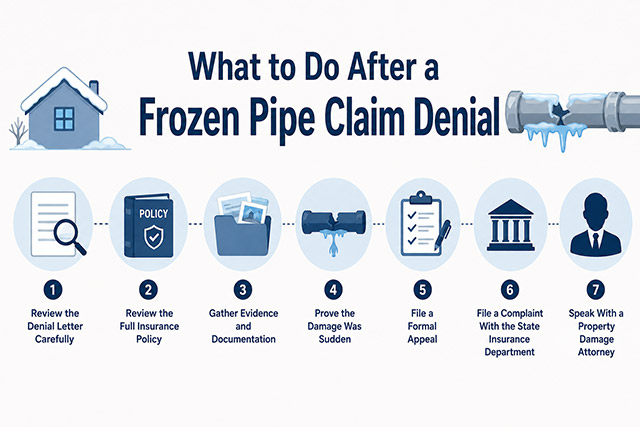

What to Do After a Frozen Pipe Claim Denial

Receiving a denial letter after dealing with a burst pipe can feel overwhelming. However, many denial disputes are not resolved with the insurer’s first decision. Taking the right steps early can help preserve important evidence and strengthen your position if you decide to challenge the denial.

Review the Denial Letter Carefully

Start by reading the denial letter from beginning to end. Insurance companies should explain why they denied the claim and identify the policy provisions they relied on when making that decision.

Pay close attention to:

- The specific reason for the denial

- Any policy exclusions cited by the insurer

- References to negligence, maintenance, or vacancy issues

- Requests for additional information

Homeowners should never rely solely on verbal statements when evaluating a denied claim. If the insurer communicated the denial verbally, request a written explanation.

Review the Full Insurance Policy

Many homeowners review only the denial letter and overlook the policy itself. That can be a mistake.

Carefully compare the insurer’s explanation against:

- The full homeowners insurance policy

- Any endorsements or amendments

- The “freezing of plumbing” provision

- Vacancy-related conditions

- Water damage coverage language

In some denied frozen pipe claims, homeowners may discover that the insurer’s interpretation of the policy differs from the actual wording.

Gather Evidence and Documentation

Supporting documentation can play a significant role when challenging a denial. Useful evidence may include:

- Photos and videos of the damage

- Thermostat records

- Utility bills showing heat usage

- Repair invoices

- Contractor estimates

- Inspection reports

A licensed plumber’s opinion may also help establish that the damage resulted from a sudden freeze event rather than long-term deterioration.

Weather records can provide additional support. Information from sources such as NOAA and Weather Underground may help document the severity and timing of the freezing temperatures.

Prove the Damage Was Sudden

Many claim disputes center on whether the loss resulted from a sudden event or a long-term maintenance issue. Homeowners should gather evidence showing that:

- The pipe burst unexpectedly

- Freezing temperatures occurred shortly before the loss

- The damage was not caused by gradual deterioration

- Inspections support a freeze-related failure

Independent inspections, weather data, and plumbing evaluations can help establish that the loss was sudden and accidental.

File a Formal Appeal

Most insurers provide a process for appealing claim decisions. A formal appeal gives homeowners an opportunity to directly address the reasons listed in the denial letter.

An effective appeal should:

- Respond to each stated denial reason

- Include supporting documentation

- Address disputed facts

- Reference relevant policy language

Providing organized evidence often creates a stronger foundation for further review.

File a Complaint With the State Insurance Department

If you believe the denial was handled unfairly, you may also submit a complaint with your state’s insurance regulator.

Homeowners in Texas and Louisiana can file complaints with their respective Departments of Insurance. While a complaint does not guarantee a different outcome, it creates a formal record of the dispute and may prompt additional review of the insurer’s handling of the claim.

Speak With a Property Damage Attorney

When significant damage or coverage disputes are involved, legal guidance may be worth considering. A property damage attorney can help homeowners:

- Review the policy language

- Evaluate the denial reasons

- Identify potential claim-handling issues

- Assess whether the insurer conducted a fair investigation

- Help challenge wrongful denials

Because insurance policies and applicable laws may contain important deadlines, homeowners should avoid waiting too long after receiving a denial letter.

A denied claim does not have to be the end of the process. By reviewing the policy, preserving evidence, and understanding the available options, homeowners may be in a better position to challenge an unfavorable decision and protect their rights.

Real Homeowner Experiences After Frozen Pipe Claim Denials

Many homeowners encounter similar challenges after a frozen pipe loss. Understanding how these disputes commonly unfold can help homeowners recognize potential issues and respond more effectively.

What Happens if the Insurance Company Denies a Frozen Pipe Claim After a Power Outage?

One of the most frustrating scenarios occurs when a homeowner loses power during a severe winter storm, only to have the insurance company later argue that they failed to maintain heat inside the property.

This issue became especially common after major freeze events in Texas and Louisiana, where widespread outages have a history of leaving thousands of homes without electricity for hours or even days. Despite those circumstances, some homeowners still received denial letters alleging negligence or failure to protect the property.

Homeowners facing a power-outage-related denial should focus on showing that the loss of heat resulted from circumstances outside their control. Utility outage reports, weather records, and communications from the power company may help demonstrate that the property lost heat because of a widespread emergency rather than homeowner neglect.

What Can Homeowners Do if the Insurance Company Delays, Underpays, or Barely Investigates the Claim?

Not every dispute involves a complete denial. Some homeowners report receiving low settlement offers, delayed responses, or inspections that appear rushed and incomplete.

Common homeowner complaints include:

- Drive-by or limited inspections

- Low repair estimates

- Delayed communication

- Repeated requests for the same documents

- Allegations that the damage resulted from wear and tear

When this happens, homeowners can request a more thorough investigation, obtain independent repair estimates, and submit additional evidence supporting the claim. Significant differences between repair costs and the insurer’s estimate may justify further review.

In some situations, repeated delays or inadequate investigations may raise concerns about whether the claim received a fair evaluation. Understanding those warning signs can help homeowners determine whether additional action may be appropriate.

What Texas and Louisiana Laws Say About Denied Frozen Pipe Claims

State law provides important protections for homeowners dealing with denied, delayed, or underpaid insurance claims. While every claim is different, understanding the basic legal framework can help homeowners evaluate whether an insurer is handling a claim appropriately.

Texas Insurance Laws

Texas law includes consumer protections designed to encourage prompt claim handling and fair investigations.

Texas law generally requires insurers to acknowledge a claim within 15 days and issue a coverage decision within 15 business days after receiving the requested information. Approved claims are generally paid within 5 business days. Texas law may also allow certain extensions under specific circumstances.

Many homeowners insurance policies in Texas contain contractual deadlines that may limit the time available to file a lawsuit. In most cases, that period may be as short as two years from the date of loss.

These claim-handling deadlines and coverage disputes frequently arise in freeze-prone areas such as Dallas, Fort Worth, Austin, San Antonio, Houston, Beaumont, and East Texas communities affected by severe winter weather.

Louisiana Insurance Laws

Louisiana law requires insurers to pay a covered claim within 30 days after receiving satisfactory proof of loss. Failure to do so without a reasonable basis may expose the insurer to penalties under Louisiana insurance law. Homeowners may also have additional legal remedies when insurers unreasonably delay claim handling or arbitrarily deny valid claims.

Frozen pipe claims commonly arise in areas such as New Orleans, Baton Rouge, Shreveport, Monroe, Lake Charles, and other parts of Louisiana that experience occasional hard freezes. Louisiana policyholders typically have two years to file claims alleging insurer bad faith practices, although the specific facts of a case can affect applicable deadlines. Because claim disputes often involve questions about coverage, documentation, and policy interpretation, timely communication and investigation remain important throughout the process.

Important Legal Deadlines

One of the biggest mistakes homeowners make after a denial is waiting too long to act, especially because important deadlines may involve:

- Policy notice requirements

- Appeal deadlines

- Documentation requests

- Contractual lawsuit limitations

- State law filing deadlines

While state law may provide up to two years for certain newer property damage claims, homeowners should review their specific insurance policy carefully. Some policies may contain “suit limitation” clauses that shorten the time available to file a lawsuit against the insurer. Because policy deadlines can sometimes shorten the time available to pursue legal action, homeowners should not assume they can revisit a denial months or years later without consequences.

How a Property Damage Lawyer Can Help With a Denied Frozen Pipe Claim

A frozen pipe claim denial often involves more than a simple disagreement over coverage. Insurers may rely on policy exclusions, maintenance allegations, or technical evidence that can be difficult for homeowners to evaluate on their own.

A property damage lawyer can assist by:

- Reviewing the policy and identifying relevant coverage provisions

- Challenging improper denials based on inaccurate facts or policy interpretations

- Addressing underpayments as well as outright denials

- Evaluating available remedies under applicable state law

- Helping homeowners avoid missed deadlines and procedural requirements

- Communicating and negotiating directly with insurance company representatives and defense counsel

Most importantly, an attorney can provide an independent assessment of whether the insurer’s position is supported by the policy and the available evidence. For homeowners facing significant property damage, this review can help clarify the options available moving forward.

Conclusion

A frozen pipe claim denial does not automatically mean you caused the damage, failed to protect your property, or lost your right to challenge the insurer’s decision. In many cases, denials are based on disputed facts, incomplete investigations, or differing interpretations of policy language rather than clear evidence that the claim is not covered.

One of the biggest mistakes homeowners make is assuming the insurance company’s first decision is final. Insurance companies often make claim decisions based on the information available during the initial investigation. That decision may not reflect the full story. When questions remain about coverage, the cause of the damage, or the insurer’s handling of the claim, a closer review may uncover options that were not apparent at the outset.

If your frozen pipe insurance claim was denied, do not wait to explore your options. Insurance policies and state laws may impose important deadlines that can affect your ability to challenge the decision. Contact Pandit Law for a free claim review and learn whether a property damage attorney can help you pursue the coverage you paid for.